The GBP/JPY currency pair is a baffling one to watch. It spiked tremendously after the US presidential elections but has consolidated in a tight trading range as it retreats beneath its 50-day moving average, and hovers around its 200-day moving average. On Monday this week, The Dragon attempted to break out above the 140 level but found too much resistance there. A rally now seems an unlikely scenario for the GBP, however, a rise above 142 would bring plenty of bullish traders into the mix.

The current support level appears to be holding at the 200-day moving average of 138.50. This level also happens to be what technical FX traders understand as the Fibonacci retracement level. On Monday, the GBP rose above the critical 140 level but found it difficult to hold that line. That the GBP/JPY pair formed a negative candle is important. The 138.50 level is what binary options trader should be targeting. This means that put options based on current trends are required.

What should you be looking for when trading on the strength or weakness of the GBP?

Today and tomorrow, it’s important to look for support at the 138.50 – 138.85 level. We are likely to see strong resistance trending in the 142.05 – 142.80 trend line, with the major resistance at 140.75. Recall that the Beast has been trading inside this current channel for 8 trading sessions on the trot. This indicates it is in a tight range and unlikely to show sudden swings in either direction. If the current downtrend continues, it will be important to look at the next lower level at 138, and then 136.45. As for the actual economic indicators in the UK, Brexit fears are causing significant volatility. Here is a snapshot of the most important UK economic indicators right now:

Related Posts

Trade Update On These 3 Stocks: AMZN, MSFT And AAPL

Trade Update On These 3 Stocks: AMZN, MSFT And AAPL- Sensex Opens Flat Ahead Of Budget 2017

2016 Market Meltdown: We Have Never Seen A Year Start Quite Like This

2016 Market Meltdown: We Have Never Seen A Year Start Quite Like This NFLX Plunges After Missing Sales, Subs And Earnings; Cuts Forecast; Burns Quarter Billion Dollars

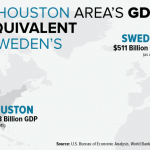

NFLX Plunges After Missing Sales, Subs And Earnings; Cuts Forecast; Burns Quarter Billion Dollars The Effects Of Hurricane Harvey

The Effects Of Hurricane Harvey- It’s The Trump Slump—But Don’t Blame The Donald!

Leave A Comment