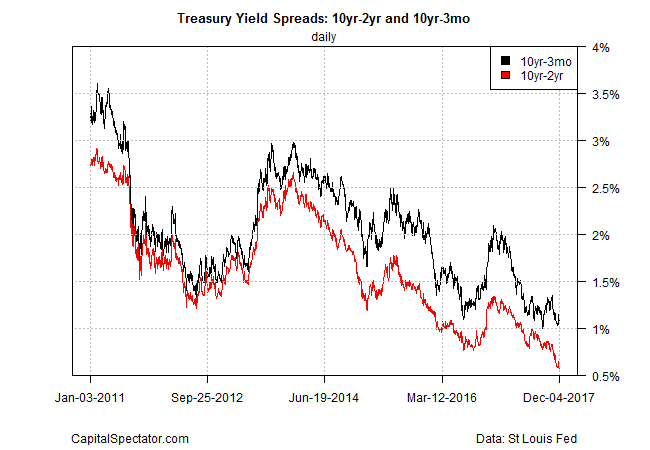

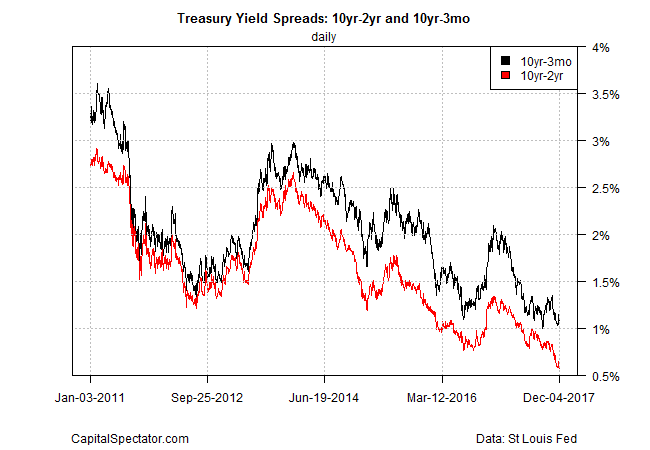

The gap between the 10-year and 2-year Treasury yields fell to 57 basis points on Monday (Dec. 4), according to Treasury.gov’s daily data. The dip marks yet another post-recession low for this widely monitored spread. The flattening of the yield curve implies that the economy is facing stronger headwinds, based on the spread’s history vis-à-vis the US business cycle. But the macro trend remains solid at the moment, suggesting that the 10-year/2-year yield gap has shed its value, at least temporarily, as an early warning of US recession risk.

Whatever the outlook for the economy, the source of the sliding 10-year/2-year spread is clear. The rate for the shorter maturity has been consistently rising since September, driven by growing confidence that the Federal Reserve will continue to raise interest rates. The 2-year rate ticked up on Monday to 1.80%, the highest since the recession ended in mid-2009. Meanwhile, the benchmark 10-year yield has been more or less flat in recent months, holding in a range of roughly 2.20% to 2.40% — below this year’s 2.62% peak in May.

Meanwhile, the week’s Fed meeting is expected to deliver another round of tighter monetary policy. The futures market for Feds funds is currently projecting an implied 90% probability that the central bank will announce a rate hike on Dec. 13, according to CME data. If the forecast is right, the Fed funds target rate will rise 25 basis points to a 1.25%-1.50% range, the highest since 2008.

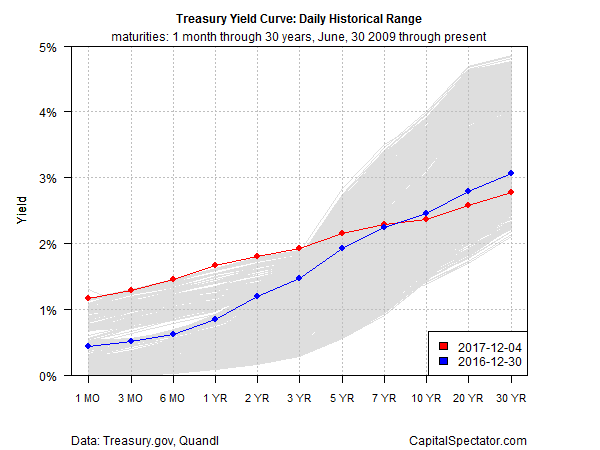

The general flattening of the Treasury yield curve is conspicuous this year for all maturities up through the five-year rate.

History suggests that a narrowing yield spread is a warning sign for the economy, particularly if the curve inverts (short rates above long rates). The 10-year/2-year spread is still positive, but with less than 60 basis points to go before inversion this spread could go negative in the near term if current trend persists.

Related Posts

Gold: Continues To Trades Below Key Resistance

Gold: Continues To Trades Below Key Resistance Towards a milder tax climate

Towards a milder tax climate Fed Household Spending Survey Projections In Firm Downtrend

Fed Household Spending Survey Projections In Firm Downtrend “Go With The Flow” – Trader Warns “The Market’s Not Ready To Be Properly Understood Yet”

“Go With The Flow” – Trader Warns “The Market’s Not Ready To Be Properly Understood Yet”- GBP, JPY: Balanced Risks S/T; Buy A GBP Dip & Sell A JPY Rally L/T – BofAML

Short Setups, But You’ll Want To Hold Off For Now

Short Setups, But You’ll Want To Hold Off For Now

Leave A Comment