After a mediocre 3Y, and a strong 10Y auction in the last two days, the Treasury concluded its refunding on the right foot – if with some blemishes – selling $15 billion in 30Y bonds at a 2.801% yield, stopping through the WI 2.802% by the smallest possible margin, and below last month’s 2.870%.

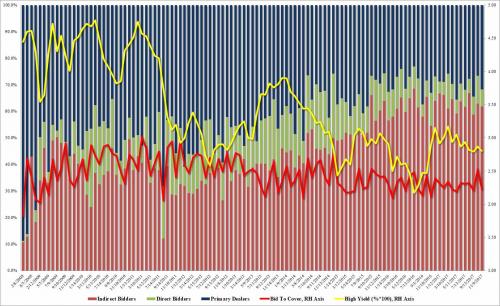

There was some weakness in the bid-to-cover which dipped to 2.23 from the previous auction’s 2.53, and below the 6 month average 2.312%. Total bids of $35.2 billion competed for $16.8b in bonds incl. $1.8 billion in SOMA, vs $30.4b in bids for $12.0b in bonds sold in the October auction.

Indirect bidders were awarded 61.8%, in line with October’s 62.8% and the 6 auction average of 61.2%. The award to directs dropped to 6.4% vs previous auction’s 10.6%, if not far off the average 6.9%, leaving dealers taking down 31.8%, above October’s 26.6%, and right on top of the recent 31.0% average.

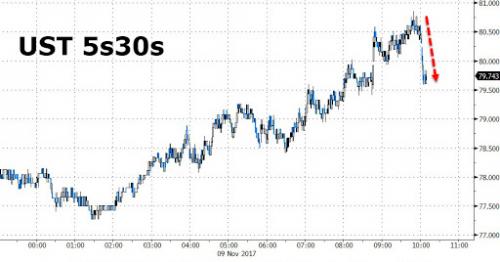

As Bloomberg commented, the “auction was expected to benefit from demand for duration that has pushed 5s30s curve to multi-year lows, favorable supply trends and short positioning by speculators in futures; while cheaper outright and on curve Thursday, sector has richened notably over past month.”

Finally, for those who follow the yield curve, it snapped lower, and back under 80bps, on the relatively strong auction.

Leave A Comment