Deutsche Bank’s chief international economist warns that inflation risk is rising, posing the main threat for the investment outlook. Some analysts disagree, although the Treasury market seems to be pricing in this risk.

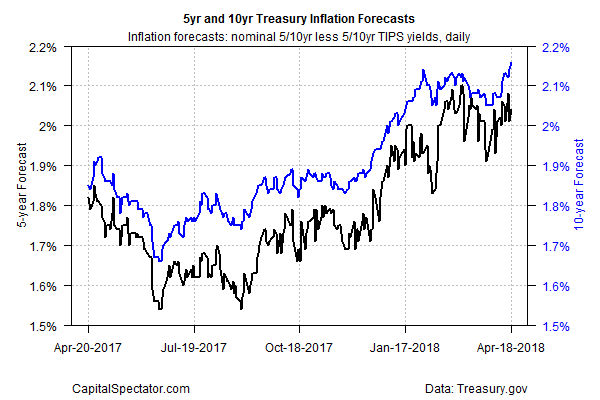

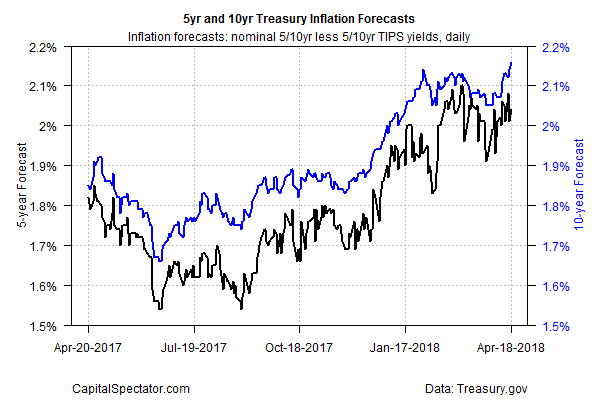

The implied inflation forecast via the yield spread for the nominal 10-year rate less its inflation-indexed counterpart ticked up to 2.16% on Wednesday (Apr. 18) – the highest since the summer of 2014, based on Treasury.gov’s daily data. That’s still a subdued level compared with the post-recession peak of roughly 2.60%. But the upside bias in recent months suggests that the unusually low inflationary tide may finally be turning.

According to Deutsche Bank’s Torsten Slok, the cat’s already out of the bag. “I think inflation is the mother of all risks here,” the firm’s dismal scientist told CNBC on Tuesday. “We’ve been waiting for inflation, literally, for the last nine years, since the recession ended in 2009. You could ask the question, ‘Well, why now? We didn’t see inflation for the last few years, so what’s different today?’”

The answer can be found in a weak U.S. dollar (the dollar index has wallowed around the 90 mark for much of 2018, after a stunning free fall in 2017), an immense fiscal expansion in the last decade pushing the economy toward overheating, a tight labor market, and recent (albeit modest) price pressure in the wake of trade war possibilities and tariff talk, Slok said.

Inflation has firmed up, but there’s still room for debate about the near-term outlook for pricing pressure. Yes, the dollar has weakened over the last year, but the slide follows the sharp 2014-2015 rally and so the US Dollar Index is unchanged relative to its close in 2014.

Keep in mind, too, that the official inflation data is relatively contained. But to Slok’s point, the upside trend appears to be gathering momentum, albeit on the margins. Notably, the year-over-year rate of core consumer inflation (excluding food and energy) ticked up to 2.1% in March, the highest in more than a year.

Related Posts

Looney Plunges As Canadian GDP Collapses Most Since 2009

Looney Plunges As Canadian GDP Collapses Most Since 2009 Grayscale CEO highlights 20% GBTC share buyback option if ETF conversion fails

Grayscale CEO highlights 20% GBTC share buyback option if ETF conversion fails- Electrical Power Consumption, Economic Growth And Global Warming

Renewable Energy Scales 52-Week High On Acquisition

Renewable Energy Scales 52-Week High On Acquisition Nike’s Kaepernick Ad Has Cost The Company Over $3 Billion So Far

Nike’s Kaepernick Ad Has Cost The Company Over $3 Billion So Far- Three Reasons Why I Don’t Like The “Policy Makers”

Leave A Comment