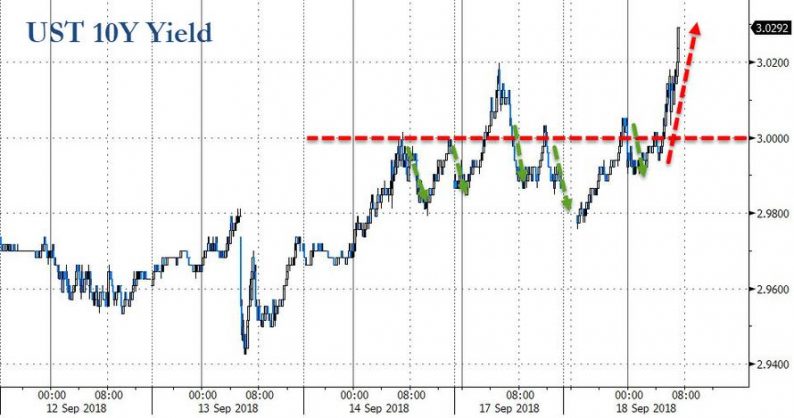

Having failed to sustain above 3.00% yesterday, the lack of immediate and aggressive response from China has hyped risk appetite this morning and sent Treasury yields notably higher – breaking to the highest since May 23rd.

Furthermore, expectations of additional China stimulus (talk of RRR cuts among other things) have also pushed yields higher…

This is the highest 10Y Yield since May 23rd…

As Goldman notes, there are a number of levels to be aware of now between 3.007% and 3.056%.

The two prior highs from June/August are up at 3.007-3.014%. The bigger level, however, is likely going to be 3.0556%; an equality target from May. Everything up to 3.0556% can still be considered corrective/counter-trend.

In other words, the market would have to break further than there to really consider the possibility of a more meaningful sell-off. Until that happens, it’s going to be very important to watch for signs of a top/turn forming there.

View: Next resistance level at 3.007-3.014%. Could reach up to 3.056% and still be counter-trend. Need above 3.056% to be considered a more meaningful sell-off.

Breakevens are spiking also on the heels of WTI’s spike after Saudi comments…

And perhaps of further note, the real 2yield curve has inverted…

As Bloomberg’s Ye Xie notes, the 10-year real yield has approached 90 bps, not far from the seven-year high of 94 bps set in May. More interestingly, the five-year real yield is now higher than 10s. In other words,the yield curve for inflation linked bonds (blue line) has inverted!

If we think of the real yield as investors’ expectations for the real neutral rate, then the market is saying the short-term neutral rate is now above the long-term. That is consistent with what Fed Governor Brainard highlighted in a recent speech. That suggests the FOMC will continue to tighten the Fed fund rate to a more restrictive level, perhaps until the nominal curve inverts as well.

Related Posts

468 Reasons To Be In Cash – But Have Your Watch List Ready For A Rally

468 Reasons To Be In Cash – But Have Your Watch List Ready For A Rally- EUR/JPY Remains The Offensive Targeting The 132.61 Level

- VIX Crunch

- “Friday ‘Shock’ Larger Than Brexit For Quants”: BofA Expects $52 Billion In Near-Term Selling Pressure

Immersion Corporation: Shares Fall On Lower Than Expected Q4 Earnings

Immersion Corporation: Shares Fall On Lower Than Expected Q4 Earnings Forget About Turkey: Asia Is The Elephant In The Room

Forget About Turkey: Asia Is The Elephant In The Room

Leave A Comment