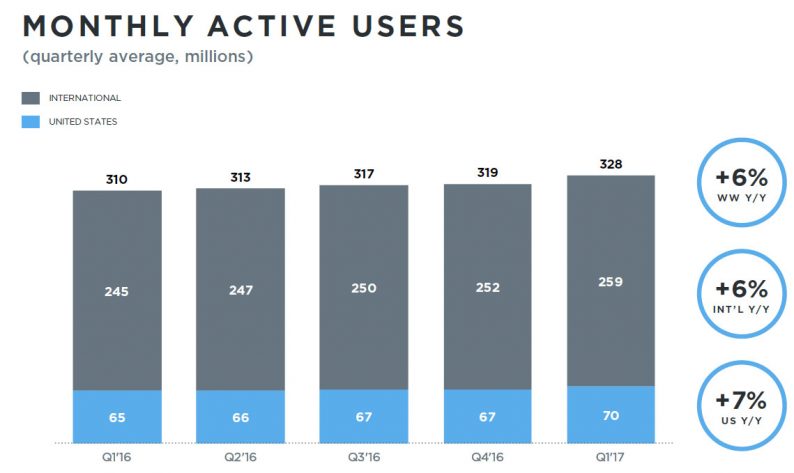

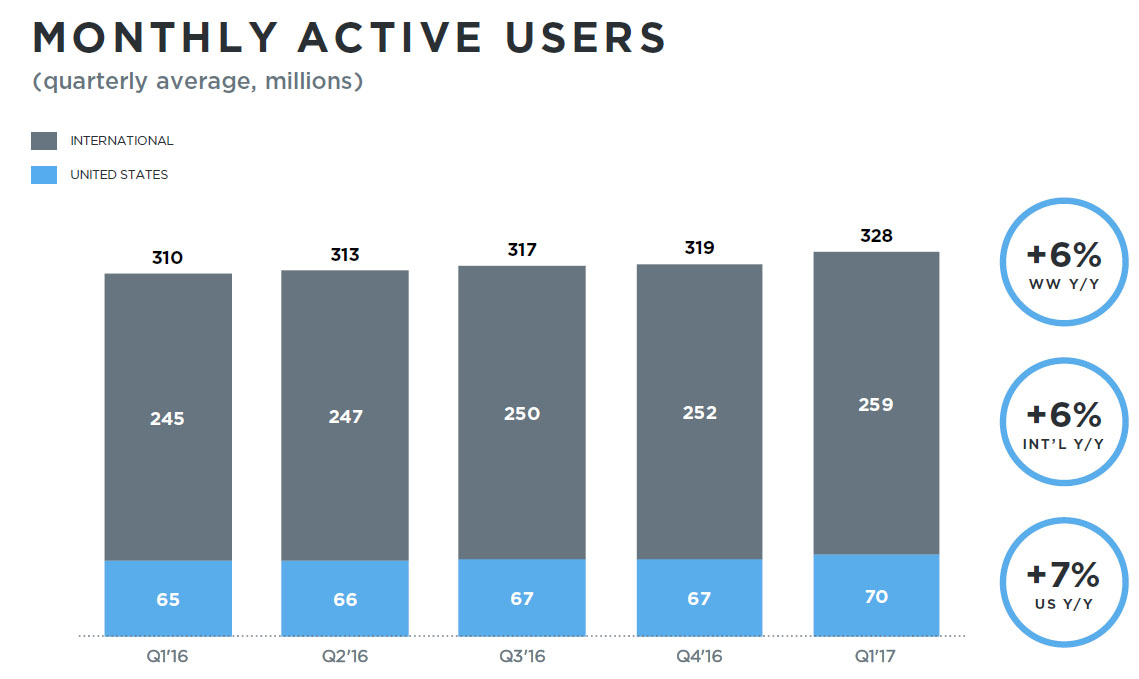

For once Twitter (TWTR) did not disappoint Wall Street, when moments ago it reported results that beat consensus estimates handily as non-GAAP EPS of $0.11 beat consensus of $0.02, even topping the highest estimate of $0.10, on revenue of $548.3 million, also beating est. of $509 million (just don’t look at the GAAP EPS loss of 8 cents). Helping the beat was a jump in monthly active users, which rose to 328 million, beating estimates of 322 million, on Q1 daily active usage up 14% y/y, higher than 11% in 4Q and 3% in 1Q16.

In kneejerk reaction the stock was up 9% in premarket trading, having risen as much as 11%.

That said, there were some less welcome signs, especially in the outlook, where Twitter expects adjusted EBITDA to be between $95 million and $115 million; below consensus est. of $137.1 million.

Some further guidance:

Just as concerning, the company still sees 2017 advertising revenue growth to meaningfully lag audience growth, further pressing the top-line growth case.

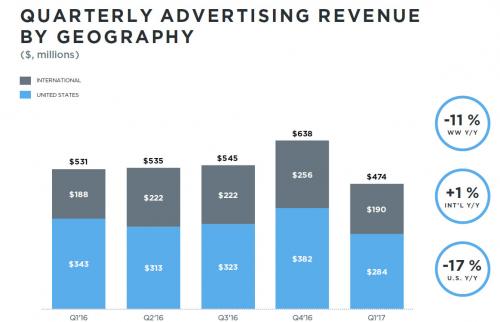

As shown in the chart below, TWTR just suffered its first revenue slowdown in Q1, with total revenues dropping 11% Y/Y.

Worse, advertising revenue in the US tumbled 17% Y/Y, a confirmation that advertisers are shifting to other social networks.

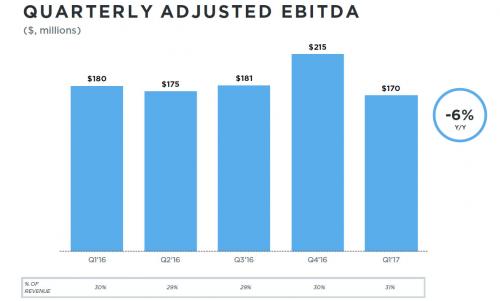

Adjusted EBITDA – which excluded $117 million in stock-based compensation – similarly declined by 6%.

How does TWTR get from net loss to adjusted EBITDA:

Leave A Comment