Forecasts for the University of Michigan Consumer Sentiment predicted the preliminary October release to increase to 100.5 from last month’s 100.1. This morning’s release missed forecasts, falling to 99.0. While this is below previous levels, it is important to note that it is not a big drop in sentiment, nor is it low relative to recent years. Admittedly not by much, the 99 level is still above the average so far in 2018 of 98.5.

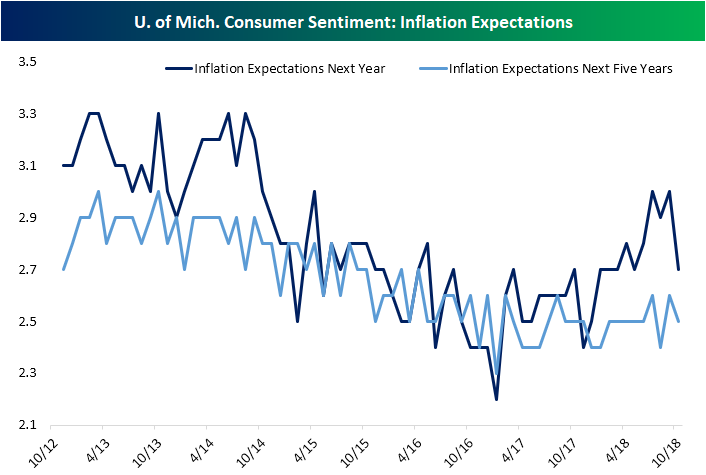

The release cited part of the reason for declining sentiment was rising inflation expectations for the next year. The chart below shows the inflation expectations for consumers that are interviewed in this survey. Consumers have had steep declines in near-term inflation expectations recently, but October’s preliminary report actually saw an increase to 2.8% from 2.7% for expectations for next year. For a longer time horizon of the next five years, expectations have fallen to 2.3%, the lowest level since December 2016 and joint-lowest of the cycle. In addition, the survey mentioned weaker real income expectations alongside declining household income growth as reasons for the weaker index number. An important matter to note concerning this release is the interviews conducted in the survey had only one night of overlap with the downturn in the markets over the past week. In other words, this preliminary release is not likely to account for any large change in sentiment from this event. When the final release comes on October 26th, we should be able to see what effect, if any, the past few days of market declines have had, and how inflation expectations pan out for the rest of the month.

Related Posts

Campbell Cuts Fiscal ’15 View Despite Strong Q1 Earnings

Campbell Cuts Fiscal ’15 View Despite Strong Q1 Earnings- Energy Stocks May Be The Next Trending Sector

EUR/USD: ‘Disorderly Times’: Where To Target? – Credit Suisse

EUR/USD: ‘Disorderly Times’: Where To Target? – Credit Suisse- New Home Sales At Interim High Of 552K

German Manufacturing PMI Misses With 58.3 – EUR/USD Ticks Down

German Manufacturing PMI Misses With 58.3 – EUR/USD Ticks Down GBP/USD Forex Signal: Bearish Consolidation Below $1.3154

GBP/USD Forex Signal: Bearish Consolidation Below $1.3154

Leave A Comment