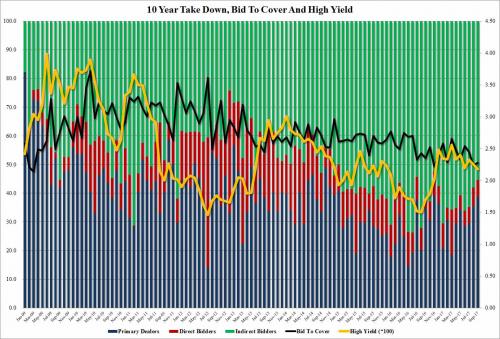

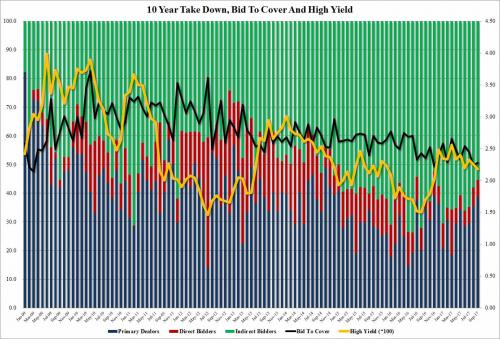

If yesterday’s 3Y auction was ugly, today’s $20 billion 9-year-11 month reopening was just as abysmal.

With a high yield of 2.18%, this was not only a whopping 1.1bp tail to the 2.169% When Issued, it was the 6th consecutive “tail” in a row, with just 2 10Y auction stopping through so far in 2017 (January and March). That said, the yield was also the lowest since November, which may explain some of the weak bidside interest.

The internals were ugly, with a Bid to Cover of 2.28, fractionally above August’s 2.23, but well below the 6 month average. Just like yesterday, foreign bidders balked, and the Indirect award was a paltry 55.3%, down from 57.9% last month, and below the 63.4% average. This was the lowest Indirect award since November 2016. With Directs once again in line, at 6.0%, just below the 6.8% last month, it was the Dealers who had to step up and they do, taking 38.7% of the final allottment, the highest since November, and well above the 29.3 6 month average.

Finally, what likely prevented today’s auction from printing notably better, is that the recent record specials in repo, which last week hit a sub-fails rate of -3.75%, was completely gone as of this morning, and the 10Y traded at 0.00% in repo at 8am on Tuesday. And with no shorts to squeeze, the result was as expected.

Leave A Comment