As the US continues to wrestle with the aftermath of the Patient Protection and Affordable Care Act of 2010 and to contemplate future changes in its health insurance programs, one useful starting point is the facts about health insurance coverage presented by Edward R. Berchick, Emily Hood, and Jessica C. Barnett of the US Census Bureau in the annual report,

Health Insurance Coverage in the United States: 2017 (Current Population Reports, September 2018, P60-264).

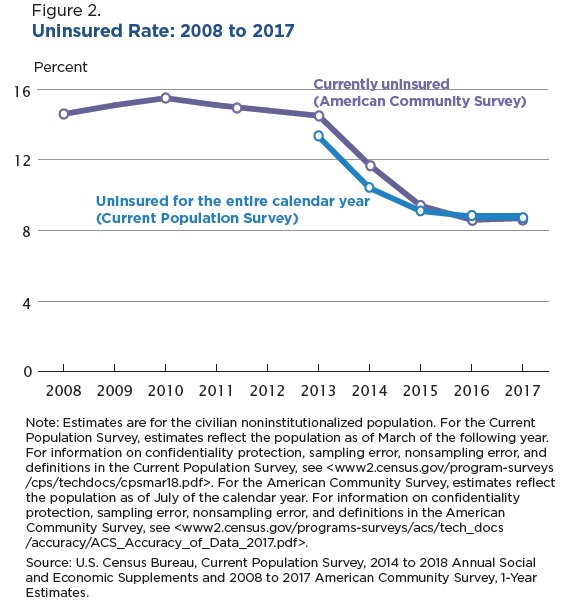

As the Affordable Care Act kicked in, it reduced the share of Americans without health insurance from 14-15% to about 8-9%.

It wasn’t a surprise that the uninsured rate remains above 8%. Before the Affordable Care Act was passed, it was not projected to provide universal health insurance. As I’ve written before, there’s no magic here about expanding coverage. The Congressional Budget Office has documented that the expansion of health insurance coverage is costing the US government about $110 billion annually. Thus, the cost of expanding health insurance coverage to an additional 20 million people works out to about $5500 per person per year. Personally, I’m fine with spending the money for this expansion of health insurance coverage, although I would have preferred to see the money raised by taxing some portion of employer-provided health insurance benefits as income.

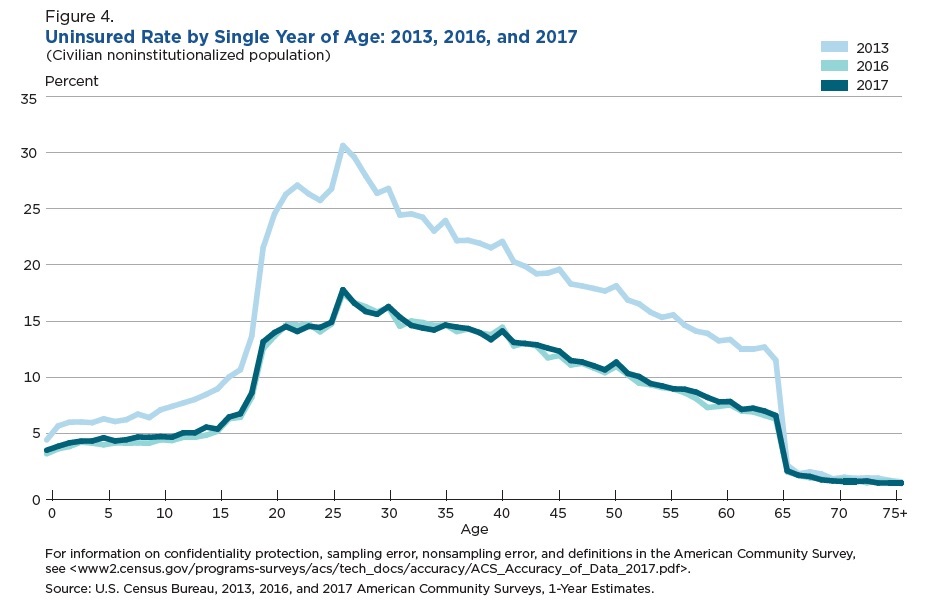

In thinking about the issue of the remaining uninsured, it’s useful to keep the age dimension of the issue in mind. This figure shows the rate of uninsured by age for 2013, 2016, and 2017. The uninsured rate for children is low (Medicaid and the Children’s Health Insurance Program) and the uninsured rate for the elderly is low (Medicare). The real spike in the share of uninsured is for young adults. Thinking about what kind of health insurance makes sense for this relatively healthy group seems potentially productive.

Another issue for the remaining uninsured is the state-level variation. This figure shows changes in health insurance coverage by state. The variations across states are substantial because states have a lot of power to determined the extent of the health insurance programs for those with low incomes. I live in Minnesota, and I’m pleased to live in a state where the share of population that lacks health insurance is fairly small. But how you feel about lack of health insurance in the US is in some ways linked to whether you can live with the idea that majorities in other states are making other choices.

Related Posts

Markets Post Across-The-Board Gains For A Fifth Week

Markets Post Across-The-Board Gains For A Fifth Week Weekly Unemployment Claims: Up 2K, Still Beats Forecast

Weekly Unemployment Claims: Up 2K, Still Beats Forecast “Failed” Bund Auction At Record Low Yield And All Other Key Overnight Events

“Failed” Bund Auction At Record Low Yield And All Other Key Overnight Events- Bear Of The Day: DuPont

Tech Wreck 2.0 Looming Over Indices, ETFs And Mutual Fund Holders

Tech Wreck 2.0 Looming Over Indices, ETFs And Mutual Fund Holders- 5 Best-Rated Goldman Sachs Mutual Funds To Invest In

Leave A Comment