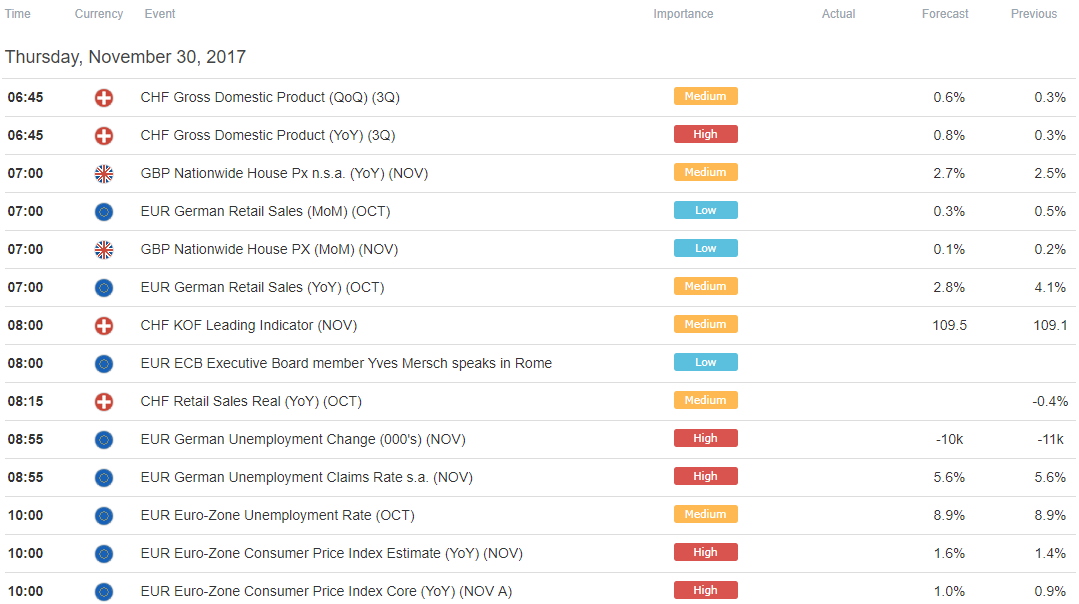

Eurozone CPI takes top billing on the European data docket, with the headline inflation rate expected to have hit a seven-month high at 1.6 percent on-year in November. Meanwhile, the German labor-market statistics are expected to leave the jobless rate unchanged at 5.6 percent while Swiss GDP figures point to accelerating growth in the third quarter.

None of these outcomes seem likely to generate a lasting response from FX markets however. ECB policy looks to be on auto-pilot in the near term, severing the link between regional data flow and the Euro. A surprise SNB policy pivot isn’t out of the question but a single data point is an unlikely trigger, leaving the SwissFranc similarly disconnected from the usual fundamental news cycle.

Fed policy speculation returns to the spotlight later in the day. The US central bank’s favored PCE inflation gauge is due, with core price growth expected to rise for a second consecutive month – the first such feat since August 2016 – to 1.4 percent. Meanwhile, a Republican-led tax cut effort will be debated and ultimately voted upon in the Senate.

With a rate hike almost certainly priced in for December’s FOMC meeting, markets have turned to the 2018 tightening path as the central point of interest. Markets expect tax cuts to be inflationary, so the US Dollar is likely to rise if the Senate votes them through. The boost may be amplified if PCE data suggests price growth is already accelerating, before fiscal stimulus enters the picture.

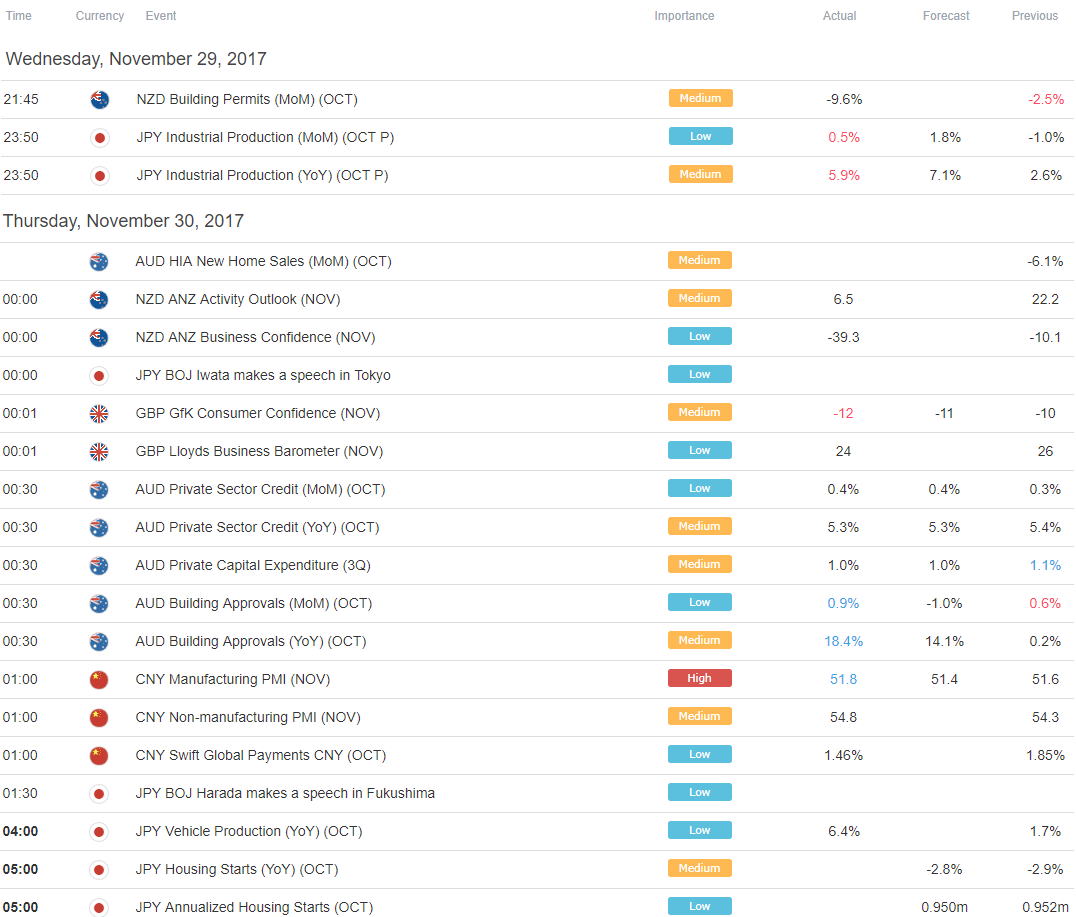

Asia Session

European Session

Related Posts

Jack Bogle Slams Wall Street’s “Unrealistic” Earnings Guesses, Says Market Valuations “Rather High”

Jack Bogle Slams Wall Street’s “Unrealistic” Earnings Guesses, Says Market Valuations “Rather High” Why Did The British Pound Stop Going Down?

Why Did The British Pound Stop Going Down? Transports- Diverging For 1-Year, Testing Important Support

Transports- Diverging For 1-Year, Testing Important Support The Top Blockchain And Cryptocurrency Power Hubs Of The World

The Top Blockchain And Cryptocurrency Power Hubs Of The World Silver Prices: Gray Metal Could Be A Better Opportunity Than Gold

Silver Prices: Gray Metal Could Be A Better Opportunity Than Gold Internet Money

Internet Money

Leave A Comment