S&P futures rebounded 0.3% from the worst two-day selloff since Sept. 2016, and European and Asian stocks rose modestly from early weakness after Trump’s SOTU address did not deliver any major surprises, while traders were cautious ahead of the Fed’s last rate decision under Janet Yellen’s leadership expected to lean on the hawkish side.

On Tuesday, U.S. stocks tumbled amid concerns about a recent sharp rally in bond yields. Health-care shares slumped after Amazon.com, Berkshire Hathaway and JPMorgan agreed to collaborate on ways to offer health-care services to their employees; drugmakers will be in the spotlight again as Trump says prescription drug prices will come down “substantially.”

Despite the recent drop, it’s been a stellar month for stock markets, with major gains across most major gauges that were followed this week by the MSCI All-Country World Index’s biggest two-day slide since September 2016. Investors will now focus on Wednesday’s Federal Reserve rate decision, the ongoing earnings season and more big economic data points to see if the uptrend can resume.

On Tuesday night, Donald Trump sought to connect his presidency to the nation’s prosperity in his first State of the Union address, arguing the U.S. has arrived at a “new American moment” of wealth and opportunity. Trump vowed the “era of economic surrender is over,” but stopped short of naming the targets of his efforts to narrow the U.S.’s ballooning trade deficit, which prevented a major market reaction.

Trump also stated the US is finally seeing rising wages and that unemployment claims have hit a 45-year low. Trump also called on Congress to produce a bill that generates at least USD 1.5tln for new infrastructure investment and said that they will work to fix bad trade deals.

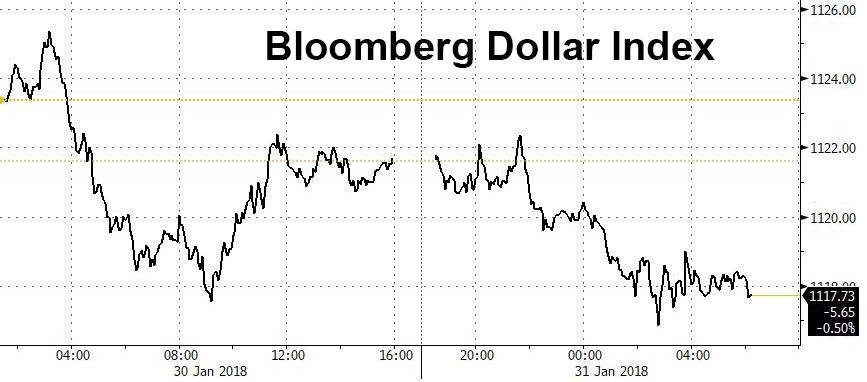

Overnight, the Dollar weakened again as Trump’s State of the Union speech offers few new details, while EMs rose as Trump failed to emphasize tariffs and trade.

“There was a moment where the dollar was bought on Trump’s infrastructure remarks, but that’s because the topic was in focus and markets reacted to that,” said Koichi Takamatsu, head of G-10 currency trading for Japan at Nomura Securities Co. in Tokyo. “On the other hand, after concerns about protectionism receded at Davos, Trump made clear his stance on ‘America First.’ Overall, the reaction to his speech was limited.”

The yen weakened as the BOJ unexpectedly boosted 3-to-5 year bond purchases in today’s open market operation and Kuroda affirmed stimulus policy, before erasing declines. Aussie grinds lower after inflation data misses, while the Aussie curve bull steepened as 3-year yield drops as much as seven basis points to 2.14% following a benign Australian inflation report. The British pound erased a gain as Prime Minister Theresa May headed to China to talk trade.

U.S. Treasuries were marginally firmer with 10-year yield just above 2.70%, despite Trump unveiling his plan for a $1.5 trillion debt-busting infrastructure plan.

European stocks erased gains of as much as 0.3%, with health-care shares (-0.5%) contributing the most to declines higher, after a two-day selloff as traders assess earnings and eye Federal Reserve Chair Janet Yellen’s final meeting on interest rates before her term ends. The Stoxx Europe 600 Index was flat heading for its best January in three years. Media shares lead gains, while Ericsson drags the tech sector lower after posting sales that missed analysts’ estimates. Capita is the biggest single-stock drag on the index after suspending its dividend and saying it plans to raise more equity, sending the stock for a record slump.

Asian stocks were mostly higher after Trump refrained from any comments that would have unnerved markets. As such, Australia’s ASX 200 (+0.2%) pared early losses and finished positive, although the commodity-related sectors continued their underperformance, while Nikkei 225 (-0.4%) swung between gains and losses with Japanese stock news dominated by earnings. Japan’s Topix index (-1.2%) slid to its lowest this year.

The region also mulled mixed Chinese Official PMI data in which Non-Manufacturing PMI topped estimates but Manufacturing PMI disappointed, which in turn disappointed local markets. The Shanghai Composite fell for a 3rd straight day, down 0.2% to 3480, while the Chinext index, tracking mid and small caps plunged near 2.7%, its biggest drop since January 15, and is now down 1% for year after rising as much as 3.7%. Big-cap blue chips outperformed with the SSE50 index tracking the 50 biggest stocks on Shanghai Stock Exchange climbed over 1.2%. The Koran Kospi index was boosted by Samsung’s stock split announcement, while the won strengthens in line with other Asian currencies. PBOC skips liquidity injections for fifth day; CSI 300 index 0.7% higher.

Of note: China’s onshore yuan climbed for its best month in at least a decade as the greenback drubbing continued. The Onshore yuan jumped 0.62% to 6.2855 per dollar in Shanghai; CNY has gained 3.5% so far in January, biggest monthly advance in CFETS data going back to April 2007 according to Bloomberg. Overnight, the PBOC weakened daily reference rate by 0.04% to 6.3339, matching average estimate in a Bloomberg survey of 25 traders and analysts; the predictions ranged from 6.3250 to 6.3414

Elsewhere, UK PM May said that there was a long-term job to do in Brexit and that she will publish Brexit impact studies during February speech in Munich. Furthermore, PM May said the UK is seeking a free trade deal with China and wants more access in the interim before trade deal. EU officials are to reject the City of London’s intention to strike a post-Brexit free trade deal for financial services, according to financial executives.

In commodities, oil retreated and industrial metals reversed losses. A measure of China’s manufacturing sector came in below expectations, while the services gauge topped estimates. WTI and Brent crude futures trade lower in the wake of last night’s larger than expected build in headline API crude oil inventories with energy newsflow otherwise relatively light ahead of today’s official EIA release. WTI crude slides below $64. In metals markets, gold prices are seen higher amid a lackluster greenback while copper was marginally supported overnight by the improvement in risk tone. Finally, Chinese steel futures were seen lower overnight as adverse weather conditions capped demand in China. Dalian iron falls two percent.

Leave A Comment