US INFLATION BEATS: 2.1% VERSUS 1.9%

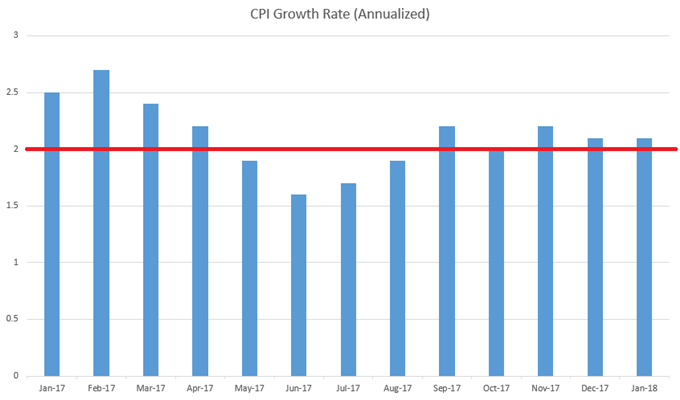

This morning brought a couple of key pieces of US data to the table, with the highlight being inflation data for the month of January. January inflation came in at 2.1% versus the expectation of 1.9%, and core inflation printed at 1.8% versus the expectation of 1.7%. This continues the theme of stronger inflationary forces in the United States, and we now have the fifth consecutive month of annualized CPI growth at or above the Fed’s target of 2%.

US CPI GROWTH SINCE JANUARY, 2017

Chart prepared by James Stanley

Also coming out in the morning and perhaps even offsetting some of the Dollar-strength around this CPI print was US Advanced Retail Sales data for the month of January. This is often thought of as being an early look into US consumer behavior as this is one of the first data points released indicating retail performance in the prior month, and this came-in below expectations, printing at -.3% versus an expectation of .2% growth.

The net response thus far has been a leap of USD strength that was quickly met by sellers, much along the lines of what we were looking at yesterday in the event that inflation came-out above expectations.

US DOLLAR VIA ‘DXY’ ONE-MINUTE CHART: RIP AND DIP ON CPI PRINT

Chart prepared by James Stanley

INFLATION IMPLICATIONS

The big concern here is one of impact, and whether or not this is something that adds additional pressure to what’s become a vulnerable backdrop across equity markets. The trigger for that vulnerability really appeared to show up as signs of stronger US inflation became more visible. In the Non-Farm Payrolls report earlier in the month, Average Hourly Earnings came-in at the strongest level since 2009. Matters haven’t really been the same since, as the following Monday saw stocks gap-down and the pressure remained for most of last week.

The premise here would be that stronger inflation brings a more-hawkish Fed, and the corresponding rise in Treasury Yields speaks to that. On the chart below, we’re looking at yields in 10-year Treasury notes, and we’re fast approaching the seven-year high at 3.04%. Perhaps the most disconcerting part of the below chart is the recent rate of change. After hovering around 2.4% for most of December, yields have posed a fast rise towards that 3% marker.

Related Posts

Xi Jinping’s Speech In Focus; L&T, ICICI Bank Among Top Stocks In Action Today

Xi Jinping’s Speech In Focus; L&T, ICICI Bank Among Top Stocks In Action Today- NFP Beats: 228K, Wages Still Stuck: 2.5% Y/y – USD Only Slightly Lower

Tips and Ideas for Opening a Gas Station

Tips and Ideas for Opening a Gas Station On Finding A Job In Finance

On Finding A Job In Finance- The Stock And Gold Markets: One’s Looking Good, The Other Not So Good

Coin98 gains 1,200% after Binance listing, Ampleforth soars on Aave integration

Coin98 gains 1,200% after Binance listing, Ampleforth soars on Aave integration

Leave A Comment