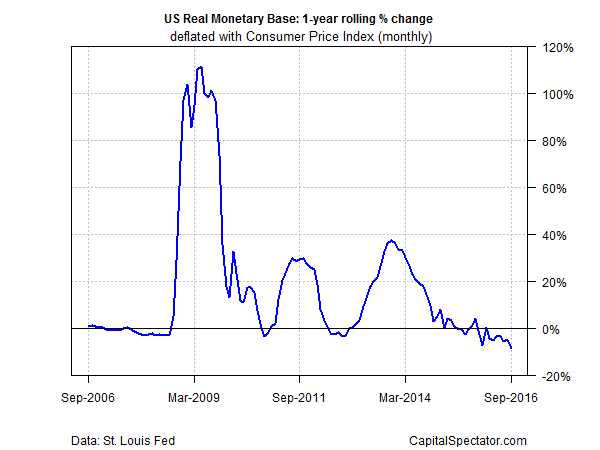

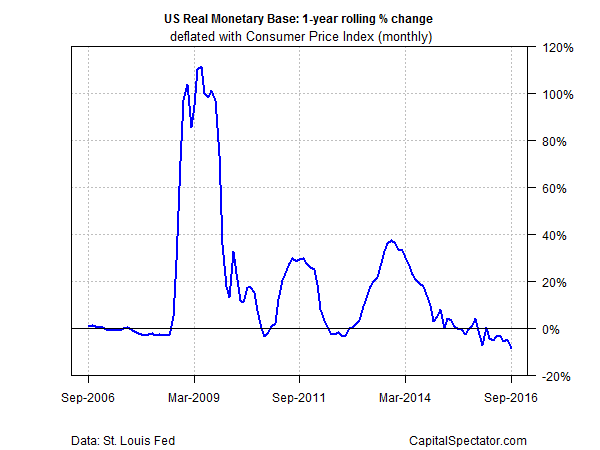

In a sign that the Federal Reserve is still on track to raise interest rates, real (inflation-adjusted) M0 money supply declined 8.8% in September vs. the year-earlier level—the steepest annual slide since 1948, based on monthly data.

Red ink for the annual trend in real M0, also known as the monetary base and high-powered money, has persisted in every monthly update this year to date save February. Taken at face value, that’s an ominous sign for the business cycle, although the outlook may be different this time.

Historically, negative year-over-year changes for real M0 have been accompanied by recessions, including the 2008-2009 downturn. As the central bank tightens monetary policy, economic growth suffers. The question is whether the analysis applies this time?

One reason for thinking that the negative M0 trend isn’t the high-risk event that it has been in the past is the extraordinarily high growth rate for high-powered money that’s prevailed in recent years. In other words, the Fed is in the process of mopping up a degree of the excess liquidity that been pumped into the system as the economy has returned to something approximating normality. As a result, the negative trend in M0 this year—the longest consecutive run of red ink since 2007, which preceded the Great Recession—may not be a prelude to a new downturn this time, at least not for the immediate future. Why? Because negative M0 growth in the current climate still leaves a relatively high amount of liquidity in the system in the wake of the Fed’s unusually aggressive monetary policy in recent years.

That, at least, is the optimistic spin on interpreting the recent M0 data. The alternative narrative is that the contraction in the monetary base is a) premature as a policy decision; b) laying the groundwork for the next recession.

Perhaps, but predicting a new downturn isn’t expected to find support in next week’s third-quarter GDP report, or so it seems via the Atlanta Fed’s current nowcast. Q3 economic growth is projected to rise 1.9% (seasonally adjusted annual rate), according to the current GDPNow estimate (as of Oct. 14). That’s a moderately higher gain compared with the sluggish growth in each of the previous three quarters.

Related Posts

The U.S. Dollar’s Dominance Is Being Challenged; It Won’t End Well

The U.S. Dollar’s Dominance Is Being Challenged; It Won’t End Well Xiaomi’s $45 Billion Valuation Seen `Unfeasible’ As Growth Cools

Xiaomi’s $45 Billion Valuation Seen `Unfeasible’ As Growth Cools Bank Of England Chief Economist Says “80 Million US And 15 Million UK Jobs To Be Taken Over By Robots”

Bank Of England Chief Economist Says “80 Million US And 15 Million UK Jobs To Be Taken Over By Robots” Gold Finds Stability After A Drop To Monthly L5 Level

Gold Finds Stability After A Drop To Monthly L5 Level- USD/JPY Looks Strong – Bounce Or Break?

- Blockchain and the evolution of business models in the game industry

Leave A Comment