Strong/ Weak Index October 10, 2017

Highlights:

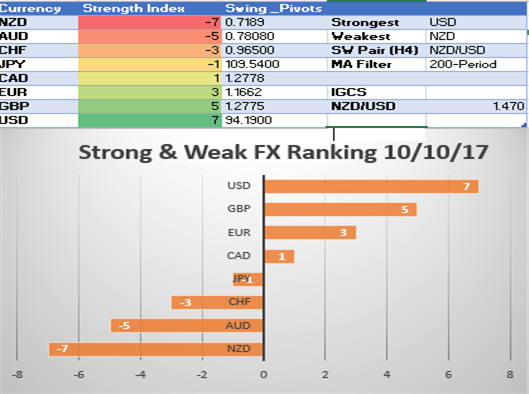

The US Dollar has lost its luster after the discounted NFP came and went. The question now remains, what will be the next catalyst to buy USD? A long-term look at the daily chart of the US Dollar Index shows the downtrend remains with a failure to close above 94.20. The price peaked above this level Friday morning but quickly closed lower. A story that has been in the background, but may soon move to the foreground is the firming Chinese Yuan, which had a stronger fixing set by the PBoC for the first time in seven days. The strengthening yuan aligns with eight straight months of higher reserves while the US 10-year note yield, which has been strongly positively correlated to the USD also looks to be running out of steam. The combination of the stronger yuan and US 10yr yields hitting resistance may seem loose, but as China’s 19th Communist Party Congress kicks off next week and US yields seem to have little reason to move higher, it’s fair to favor this ST trend of USD weakness to continue.

Quietly, the Japanese Yen has begun climbing from the bottom of the SW ranking to the middle alongside the Canadian dollar, which is also bouncing. The strength of the Japanese Yen has been forecasted by the options market, which has seen an impressive increase in open interest on options that expire on Oct. 22, which is the date of the snap election called by Shinzo Abe. While the consensus view remains for Abe remaining in power, it’s fair to keep an eye on the new Party of Hope, led by Tokyo Governor Yuriko Koike. Any ground gained by Koiki remains the outlier to watch, but overall, any significant loss of majority by Abe could lead to JPY volatility that would likely see JPY strength on uncertainty-bred repatriation.

Over the summer, Deputy Governor of the BoC, Carolyn Wilkins was the first governor to signal a BoC rate hike. Speaking on Tuesday, she will be looked at to provide a sense of the BoC’s thoughtprocess going forward. Recently, PIMCO and Blackrock have said they believe the BoC is done hiking. Given the ~60% pricing in of a rate hike, this would come as a shock to the market if Wilkins confirmed something similar. Recently, BoC governor Stephen Poloz mentioned that the bank of was not looking to hike blindly, but would remain data dependent. This comment was enough for a few-weak handed CAD-longs to bail on the trade and push USD/CAD up to 1.2600 eventually. They key thing to keep an eye on will be the trend of CAD economic data, which has recently been weak alongside correlated market like crude oil.

EUR strength is on the rise after German exports strongly beat estimates of 1.1% with a print of 3.1% m/m for August. EUR/USD has fallen from the early September high by ~3.5% to a lot of 1.1670 for a drop of 435 pips. The weakness aligned with the bounce in the DXY, which as mentioned above may be running out of catalysts along with concerns voiced by ECB members concerning the FX level (i.e., the EUR was seen as strengthening to the point of constraining growth.) The focus remains on whether or not markets will see policy convergence. Any failure for normalization to be realized by the ECB in their upcoming policy announcement could put a lid on EUR growth unless the gains come at the expense of other currencies weakening.

Markets Build On Breakouts

Markets Build On Breakouts Apple Widens The Gap On Alphabet

Apple Widens The Gap On Alphabet E

Synta Pharmaceuticals Drops Phase 3 Lung Cancer Trial

E

Synta Pharmaceuticals Drops Phase 3 Lung Cancer Trial Yuan Slides After Quadruple Whammy China Data Miss: GDP Both Matches And Misses

Yuan Slides After Quadruple Whammy China Data Miss: GDP Both Matches And Misses One Hedge Fund CIO’s Conversation With His Uber Driver

One Hedge Fund CIO’s Conversation With His Uber Driver Premier Inn to Grow Hotel Room Count by 25% Before 2030

Premier Inn to Grow Hotel Room Count by 25% Before 2030

Leave A Comment