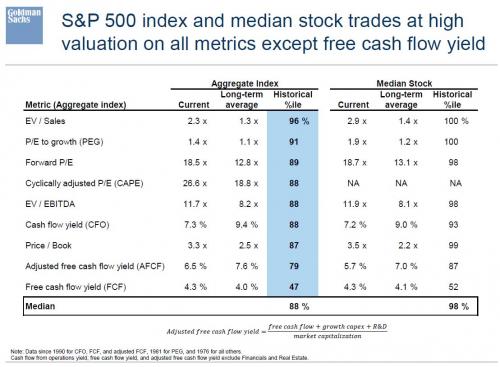

Whether it is because bond yields finally broke out of 6 month ranges, due to nerves ahead of tomorrow’s ECB tapering announcement, because the SNB is taking a long lunch break, or simply because investors finally realized that stocks have never been more expensive…

… but something odd is taking place today: selling, and nowhere is it more obvious than in the VIX ETN complex, where the VXX is suddenly caught in a vicious short squeeze.

… as the VIX is spiking, up 1.5vols to 12.63 and rising fast.

And while we recently showed that gross Vega outstanding on levered and inverse VIX derivatives including ETNs and ETFs has never been higher…

…as everyone scrambles to buy S&P calls at a rate not seen since 2007…

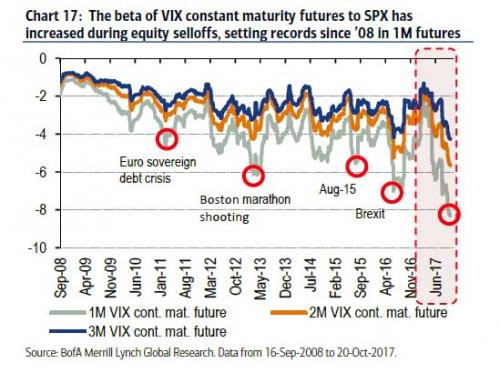

… here a rather striking update: as of today, the beta of VIX constant maturity futures to the S&P has been increasing during every previous selloff even as the VIX itself has crashed to record lows, and as of this moment, the beta on the vol index has never been higher. Here’s Bank of America looking at various VIX constant maturity futures for 1M, 2M and 3M contracts:

we’ve discussed how VIX constant maturity futures have become more reactive to S&P 500 selloffs than they were historically. The relationship continues to be pronounced, though it is most notable in the front part of the curve as the beta of the 1M VIX constant maturity future and the S&P is now -8.33, the most negative we’ve seen dating back to Sep-08. Furthermore, the betas of the 2M and 3M contracts are also at record levels versus the S&P 500 at -5.65 and -4.26 respectively.

And here’s the punchline: it’s also worth noting that the beta of the VIX spot index to the S&P is currently -18.99, also a record since Sep-08.

Related Posts

Monetary Easing Tends To Be Contagious And No Quick Fix

Monetary Easing Tends To Be Contagious And No Quick Fix Binary Options Asset Insights – July 15, 2016

Binary Options Asset Insights – July 15, 2016 CareDx – Chart Of The Day

CareDx – Chart Of The Day- What The Bulls Didn’t Want To See Friday (But We Knew Was Coming)

Aussie Dollar Faces Perfect Storm Of Domestic, External Pressure

Aussie Dollar Faces Perfect Storm Of Domestic, External Pressure The Dow Positioning Itself To Breakout In 2016?

The Dow Positioning Itself To Breakout In 2016?

Leave A Comment