One of the hallmarks of a Bull market is climbing a “Wall of Worry”. Certainly there is plenty of longer term optimism with Consumer and Small Business surveys showing extreme confidence. Yet analysts seem increasingly focused on what might go wrong.

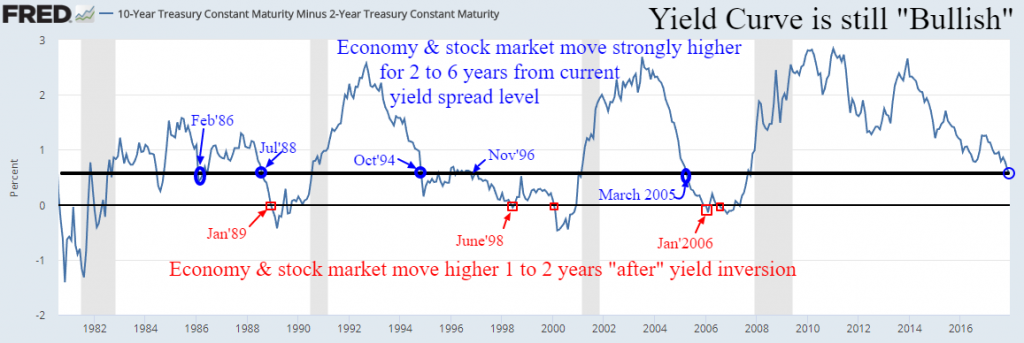

In the early days of 2009 – 2012 most were certain that the Trillions in money printing by central banks would cause massive inflation and thus contraction level node-bleed interest rates. Recently the worry du jour has been on rising short term rates that is spiraling our Yield Curve towards inversion. It’s perhaps too widely know that Yield Curve inversion has always given an accurate warning of impending economic recession months later. In “waiting for the curve” too many investors are cautious well before some unforeseeable inversion turning point.

This chart clearly shows that historically the “current” Yield Curve is not a concern, in fact it will remain a positive factor as we approach inversion. Furthermore, even after the ominous flat yield spread is reached where short term rates are equal to or above long term yields, we often witness another year or more of positive growth before recessionary contraction pressures break the back of the expansion phase. Based upon history we have at least a couple years of expansion before push come to shove in halting this 8+ year growth period.

We need to be cautious even about the merit of the yield curve if and when it does invert this time given the unusual influence of Central Banks adding reserves as never before. It should always be remembered that Central Bank efforts to flatten the yield curve, first in the US and later in Europe/Japan, are mostly an effort to regain some policy arrows to shoot back into the market in the form of lower rates and massive money printing at the first sign of any new economic contraction.

Related Posts

Continued Muted Moves For The Metals

Continued Muted Moves For The Metals- BEA Leaves 2nd Quarter 2018 GDP Growth Essentially Unchanged At 4.16%

World-Class Profitability At Carlsberg Brewery Malaysia

World-Class Profitability At Carlsberg Brewery Malaysia- Tim Cook says he bought crypto, but rejects Apple adding it to its portfolio… for now

Price analysis 11/13: SPX, DXY, BTC, ETH, BNB, XRP, SOL, ADA, DOGE, LINK

Price analysis 11/13: SPX, DXY, BTC, ETH, BNB, XRP, SOL, ADA, DOGE, LINK 5 REITs Increasing Dividends In April

5 REITs Increasing Dividends In April

Leave A Comment