Well, it’s Tuesday and everyone is frozen in time ahead of tomorrow’s CPI print.

That number would have been closely-watched even without the events of the last two weeks, but after learning just how acute the situation can get when someone screams “INFLATION!” in crowded theatre, market participants are now looking at tomorrow’s data as something of a make or break moment.

And they may be right, at least in terms of the short-term outlook for bond yields. If CPI misses to the downside, it could arrest the bond rout for the time being and while you’d be inclined to think that would be good for stocks in light of recent events, Bloomberg’s Mark Cudmore reminds you that “it could be argued that that event is skewed to be an equity negative either way.”

“If there’s high inflation, then yields might rise again, further squeezing liquidity and financial conditions,” Mark writes on Tuesday morning. “A low print — and it would appear markets have got way too far ahead of themselves in pricing rising inflation — and more wealth destruction will come through a squeeze of the large short positions in Treasuries.”

Still, over the long-term, it’s becoming increasingly difficult to argue that that yields won’t rise further. The fiscal backdrop supports that thesis as does the data, even as signs of upward pressure on prices are still nascent. And then there’s everything outlined here over the weekend.

“As QE gets tapered through this year and into next year, we’ve got a big swing in the supply duration coming,” Goldman Asset Management’s Philip Moffitt said in an interview today, adding that “I would think that 3.5 percent is not a very brave forecast.”

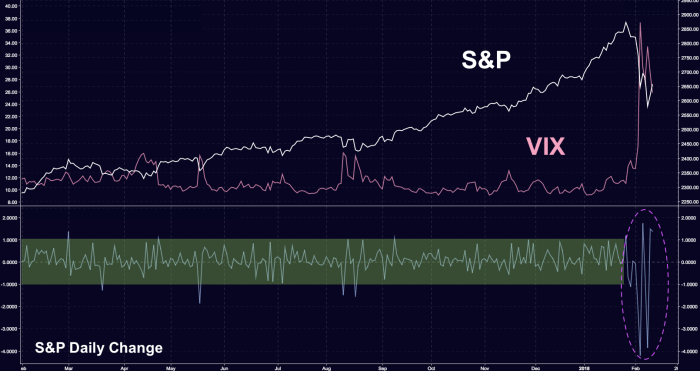

Anyway, what we do know is that “we’re not in Kansas anymore” when it comes to the daily swings.

The above-mentioned Mark Cudmore talks a bit about that on Tuesday morning as well, noting that to a market which has become accustomed to minimal moves in either direction, this looks like some crazy s**t. “February has already seen the S&P 500 carve out a range of more than 10% and we’re still less than two weeks in,” he writes, adding that “bulls shouldn’t relax until E-mini futures break above last week’s open at 2,757 while bears must be nervous about the possibility that 2529 will be seen as an important double-bottom in hindsight.”

Related Posts

Sentiment Supportive Of Further Equity Gains

Sentiment Supportive Of Further Equity Gains Dow Fails To Hold 23,000 As Yield Curve Carnage Continues

Dow Fails To Hold 23,000 As Yield Curve Carnage Continues Ethereum market cap hits $337 billion, surpassing Nestle, P&G and Roche

Ethereum market cap hits $337 billion, surpassing Nestle, P&G and Roche Rethinking Long-Term Care Policies: Will Your Health-Care Insurer Outlast You?

Rethinking Long-Term Care Policies: Will Your Health-Care Insurer Outlast You? USD/CAD At Low Support Following The Libyan Pipeline Blast

USD/CAD At Low Support Following The Libyan Pipeline Blast The Economy’s Performance Under Trump Is Not The Same Thing As His Policy Agenda

The Economy’s Performance Under Trump Is Not The Same Thing As His Policy Agenda

Leave A Comment