Financial bubbles are the office Christmas parties of the investment world. They start slowly, with a certain amount of anxiety. But they end wildly, with acts and decisions that in retrospect seem really, really stupid.

Millions of people out there still bear the psychic scars of buying gold at $800/oz in 1980 or a tech stock at 1,000 times earnings in 1999 or a Miami condo for $1,000 per square foot in 2006.

Today’s bubble will leave some similar marks. But where those previous bubbles were narrowly focused on a single asset class, this one is so broad-based that the hangover is likely to be epic in both scope and cumulative embarrassment.

This series will create a paper trail for the morning after, starting with a truly amazing anomaly: European junk bonds now yield less than US Treasury bonds.

(Financial Times) – High-yield debt belies its name as loose central bank policy skews credit markets The European high-yield market has seen €82bn of new issuance so far this year.

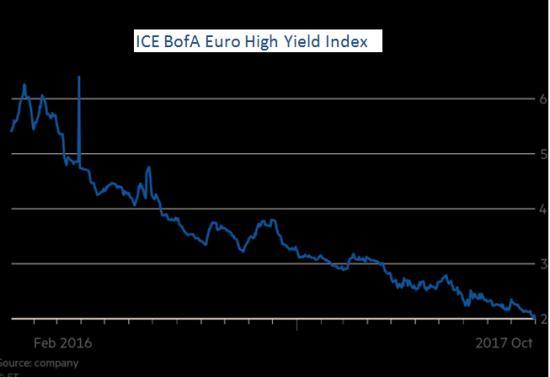

A widely tracked index of European junk bonds is on the verge of breaking below the 2 per cent yield barrier for the first time, the latest indication that loose central bank policy has skewed credit markets.

The so-called “yield-to-worst” on ICE Bank of America Merrill Lynch’s euro high-yield index slipped to just 2.002 per cent on Thursday, an all-time low for what is the most commonly used benchmark in the European junk bond market.

The index is comprised of debt sold by companies whose credit ratings are on average below the investment grade threshold. The yield on the index was as high as 6.4 per cent as recently as January 2016, when a global sell-off in riskier assets severely knocked demand for European high-yield bonds.

Shortly after that, in March 2016, the European Central Bank announced it would buy investment grade rated corporate bonds under its quantitative easing programme for first time, kick-starting a strong rally in European credit.

The central bank has since purchased over €100bn of corporate bonds, which investors say has pushed investment grade bond fund managers to increasingly buy double-B rated bonds — the highest-rated category of junk bond. These double-B bonds make up around three-quarters of the European high-yield index.

“It’s really the double-Bs that are skewing the index, particularly after the latest ECB meeting,” said David Newman, head of global high yield at Allianz Global Investors. While the index’s yield is the lowest its ever been, the spread over government bonds is still higher than at the peak of the last credit boom. The index offers 240 basis points over government bonds at present, compared with just 178 basis points in mid-2007.

ICE BoAML’s euro double-B index offers a spread over government bonds of just 197 basis points, however. Mr Newman said analysis from Allianz shows the so-called “illiquidity premium” that investors usually demand to hold riskier high-yield paper has been closer to 300bp historically. “So at current double-B spreads you’re not being compensated for the illiquidity premium, let alone any defaults,” Mr Newman said. “There’s no margin for error basically.”

The collapse in yields has spurred record issuance of European high-yield bonds with Italian telecommunications group Wind Tre last week selling the largest euro junk bond on record.

The European high-yield market has seen €82bn of new issuance so far this year, according to JPMorgan credit analysts, which they note is “within touching distance” of the previous full-year record of €84bn set in 2014. The analysts add that the net supply figure is “still subdued”, however, particularly as a red hot market for leveraged loans has seen many companies replaced their bonds with loans instead.

Many investors are worried that this squeeze on net supply is spurring excessive risk taking, with a string of formerly distressed companies in the volatile retail sector recently raising new bonds, for example. “We’re going to break through 2 per cent on the index any day now,” said a credit analyst at an asset manager. “It’s difficult to be bearish in this market and unfortunately people are getting rewarded for being long the riskiest credits.”

Related Posts

Financial Choice Act, FOMC Preview And Gold

Financial Choice Act, FOMC Preview And Gold- Richmond Fed Region Negative Again; Inventories Suggest Outright Disaster On Horizon

- Indian Indices Continue Downtrend; Capital Goods And Banking Stocks Witness Selling

- Santa’s Stock Market Rally: Tears Of Joy, Or Just Tears?

Rail Week Ending 19 December 2015: Rail Sliding Deeper Into Recession

Rail Week Ending 19 December 2015: Rail Sliding Deeper Into Recession- Don’t Miss Out On This Rare Chance To Earn A 17% Yield

Leave A Comment