Stocks were due for a breather. Last week they finally got it.

Of course, in this unusual environment that dishes out extremes (and often unfettered) rallies and pullbacks, last week’s weakness also poses the distinct possibility that a much bigger correction is now underway. The market did, after all, bump into a well-established ceiling. On the other hand, Friday’s tumble left the door wide open to a quick rebound early this week.

We’ll show you how and why below. First, let’s take a look at last week’s economic news and preview this weeks. With earnings season winding down, a couple of this week’s data nuggets have the potential to be the big market movers.

Economic Data

Last week was rather light in terms of economic announcements. In fact, there was only one data set of interest, but it was a biggie… July’s inflation data. It’s still on the rise, for consumers as well as producers. In fact, it’s continuing to press onward and upward to concerning levels.

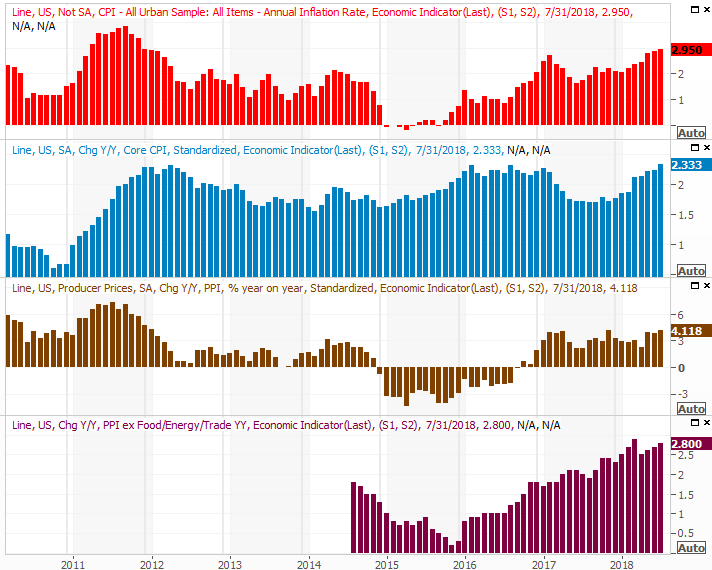

Inflation Charts

Source: Thomson Reuters

As of the latest look, the overall, annualized consumer inflation rate is 2.95%. That’s the highest it’s been since 2011. Though the root cause of the rise in inflation is a strengthening economy, the Fed has little choice but to proceed with its planned rate hikes.

Everything else is on the grid.

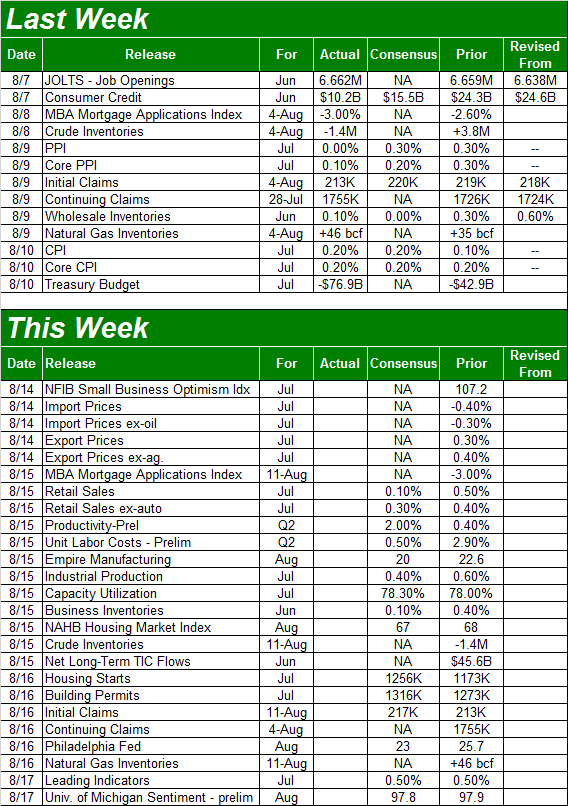

Economic Calendar

Source: Briefing.com

This week is going to be considerably busier. We’ll only be able to preview the highlights.

The party starts on Wednesday, when we’ll hear about last month’s retail spending. Sales are once again expected to rise, with or without automobile sales factored in. The ongoing improvement in consumerism bodes well for the U.S. economy, which is two-thirds driven by consumers rather than corporations.

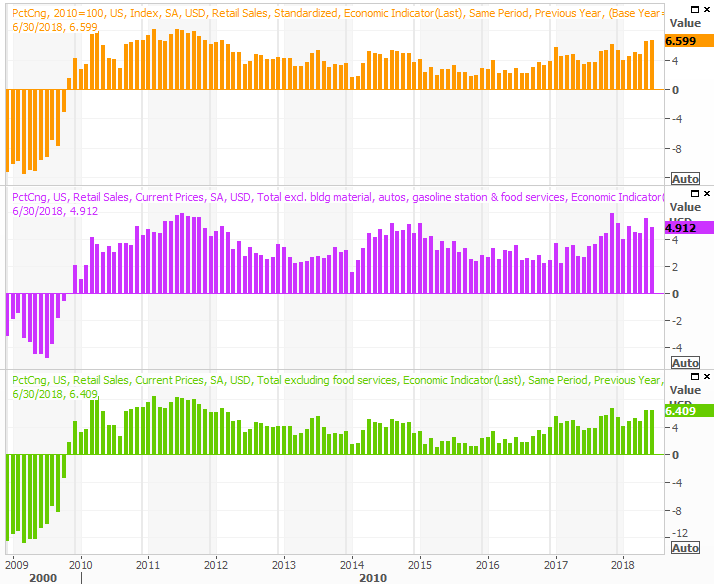

Retail Sales Charts

Source: Thomson Reuters

Related Posts

Crude Oil Prices May Fall As Gold Gains Amid Risk Aversion

Crude Oil Prices May Fall As Gold Gains Amid Risk Aversion- Calm Before The Storm

- EUR/USD Bounces, USD/JPY Breaks Ahead Of Big Week For Central Banks

Post-Lehman Legacy And Gold

Post-Lehman Legacy And Gold- RUNE rally: A closer look at THORChain’s new synthetic assets

- Courage To Act; Reflections On Fed Hubris; What If Whatever It Takes Is Not Enough? Fed Troika?

Leave A Comment