Here is the opening statement from the Department of Labor:

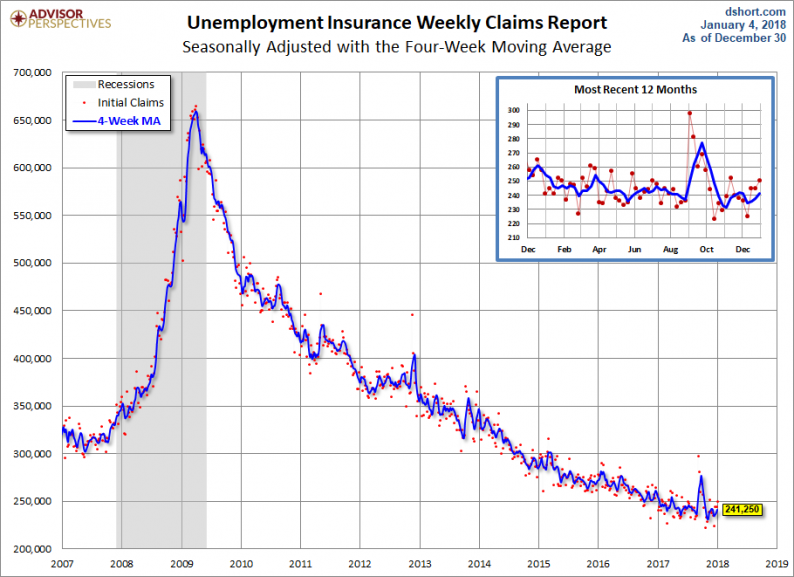

In the week ending December 30, the advance figure for seasonally adjusted initial claims was 250,000, an increase of 3,000 from the previous week’s revised level. The previous week’s level was revised up by 2,000 from 245,000 to 247,000. The 4-week moving average was 241,750, an increase of 3,500 from the previous week’s revised average. The previous week’s average was revised up by 500 from 237,750 to 238,250.

Claims taking procedures continue to be disrupted in the Virgin Islands. The claims taking process in Puerto Rico has still not returned to normal. [See full report]

Today’s seasonally adjusted 250K new claims, up 5K from last week, was worse than the Investing.com forecast of 241K.

Here is a close look at the data over the past few years (with a callout for the past year), which gives a clearer sense of the overall trend in relation to the last recession.

As we can see, there’s a good bit of volatility in this indicator, which is why the 4-week moving average (the highlighted number) is a more useful number than the weekly data. Here is the complete data series.

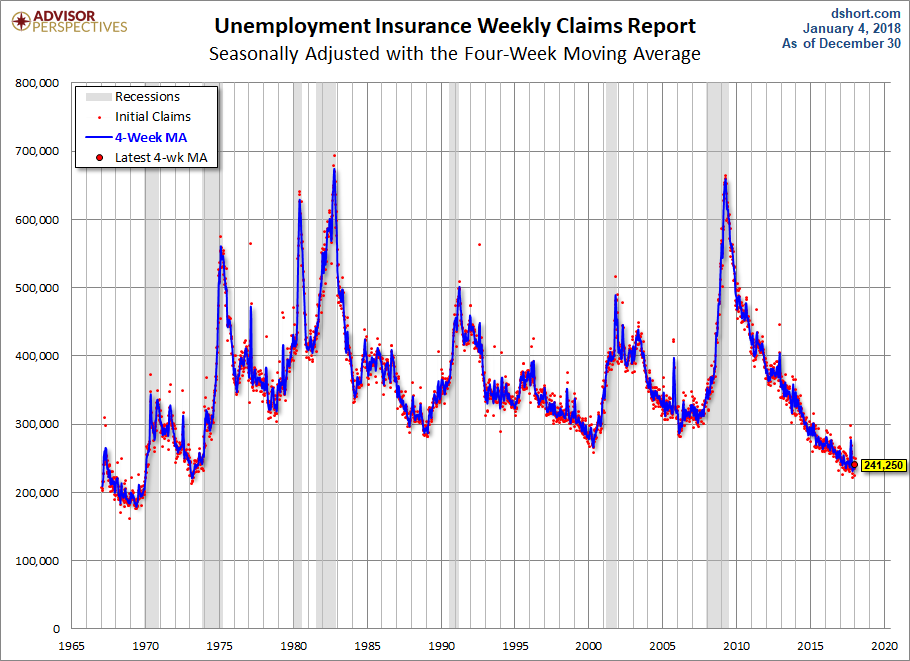

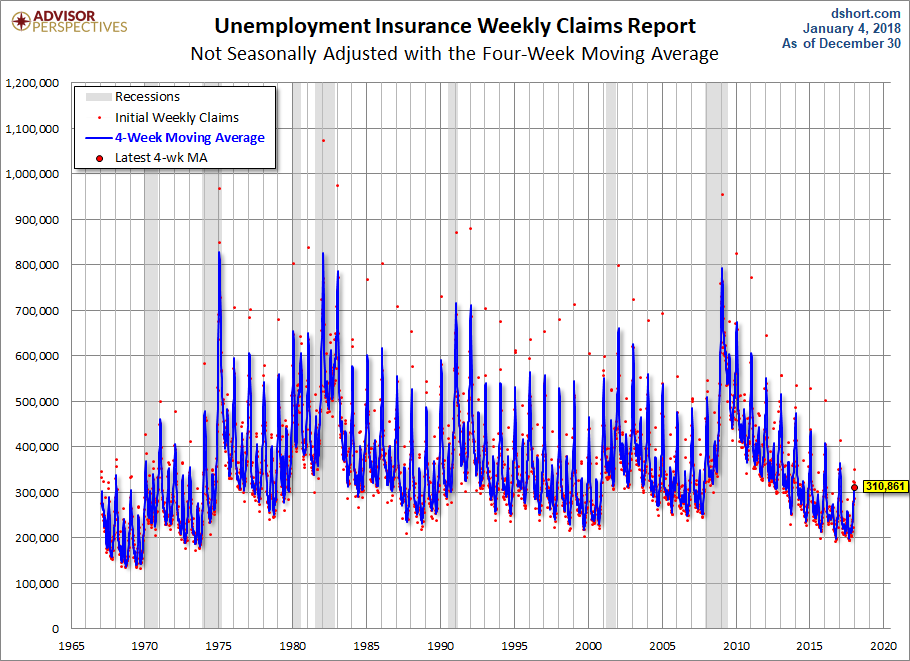

The headline Unemployment Insurance data is seasonally adjusted. What does the non-seasonally adjusted data look like? See the chart below, which clearly shows the extreme volatility of the non-adjusted data (the red dots). The 4-week MA gives an indication of the recurring pattern of seasonal change (note, for example, those regular January spikes).

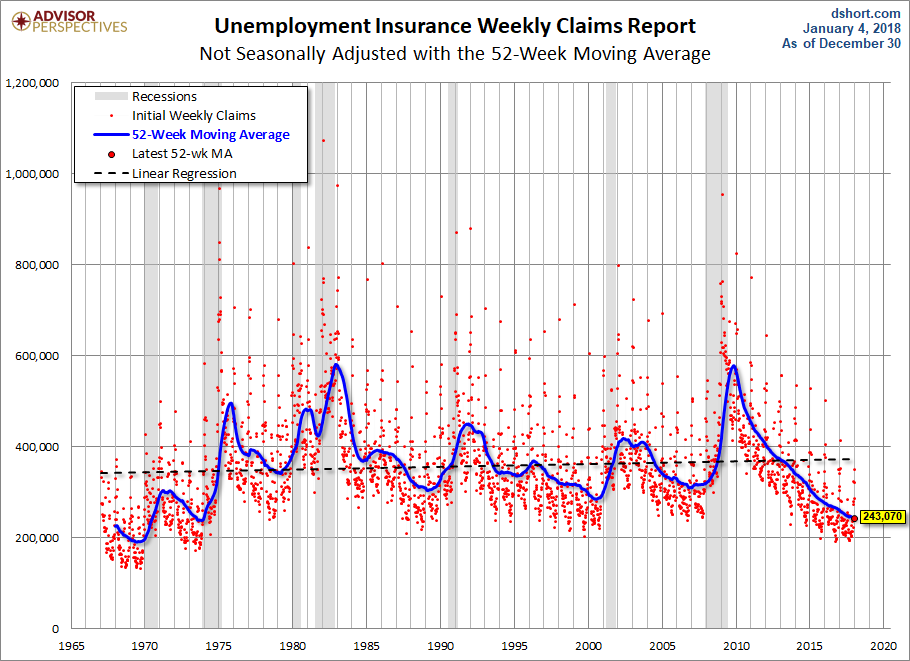

Because of the extreme volatility of the non-adjusted weekly data, we can add a 52-week moving average to give a better sense of the secular trends. The chart below also has a linear regression through the data. We can see that this metric continues to fall below the long-term trend stretching back to 1968.

Annual Comparisons

Here is a calendar-year overlay since 2009 using the 4-week moving average. The purpose is to compare the annual slopes since the peak in the spring of 2009, near the end of the Great Recession.

Related Posts

Stocks And Precious Metals Charts – Autumn – FOMC And Comex Option Expiration Next Week

Stocks And Precious Metals Charts – Autumn – FOMC And Comex Option Expiration Next Week Daily Market Outlook – Friday, October 27

Daily Market Outlook – Friday, October 27 Small Caps Head South, Large Caps Drift Lower

Small Caps Head South, Large Caps Drift Lower End Of Day Rally?

End Of Day Rally? E

Canadian Inflation Spiked Higher In July, But Core Inflation Is Right On The Bank Of Canada’s Target

E

Canadian Inflation Spiked Higher In July, But Core Inflation Is Right On The Bank Of Canada’s Target Higher Treasury Yields Point To A Rate Hike Next Week

Higher Treasury Yields Point To A Rate Hike Next Week

Leave A Comment