The economic calendar is normal, with an emphasis on housing. Earnings season begins in earnest, with widespread, high expectations. Especially after Friday’s selloff, many will be wondering: Do stock prices already reflect strong earnings growth?

Last Week Recap

In my last edition of WTWA I asked whether the Trump Trade had reached a tipping point. That was a good guess, since the week was filled with sharp market moves driven by hints, tweets, comments, and speculation about each. Each day there was a different explanation:

Monday – Trump officials walking back some of the China rhetoric. News of an FBI raid on Michael Cohen’s office seemed link to last-hour selling.

Tuesday – Chinese President Xi Jinping’s speech at the Boao Forum was interpreted as conciliatory. Overnight futures had already rebounded from the late selling but moved much higher on the news.

Wednesday – President Trump warned that a strike against Syria was imminent.

Thursday – Seemed to confuse even the punditry. You can always spot this when they start using “delayed reactions” and a sudden burst of worry about an old issue.

Friday – Strong start from bank earnings turned into selling attributed to “…some geopolitical angst prompted investors to take some money off the table ahead of the weekend”.

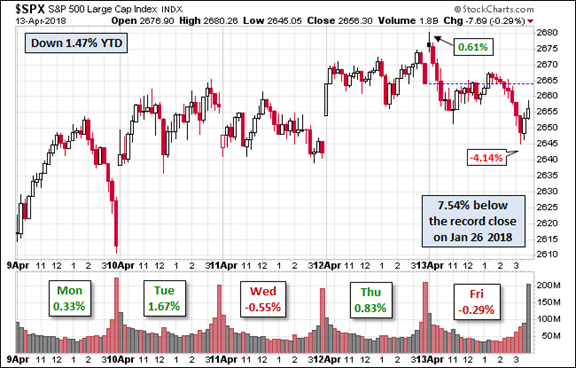

These twists and turns are apparent in the chart below. I doubt that “investors” had much to do with them!

The Story in One Chart

I always start my personal review of the week by looking at a great chart. I always start my personal review of the week by looking at a great chart. I especially like the version updated each week by Jill Mislinski. She includes a lot of valuable information in a single visual. The full post has even more charts and analysis, so check it out.

The gain for the week was about 2%, and the trading range was a bit smaller than it has been in recent weeks. I summarize actual and implied volatility each week in our Indicator Snapshot section below.

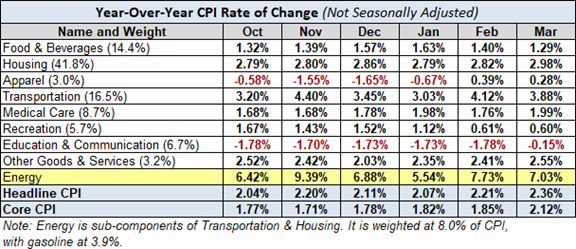

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too. WTWA is not about long-term concerns like debt. These are important, of course, but not our weekly subject unless there has been some major change.

The Good

The Bad

Related Posts

Union Pacific – Margins Improved Despite Sluggish Volumes

Union Pacific – Margins Improved Despite Sluggish Volumes Back When Things Happened In August

Back When Things Happened In August The rise of crypto charities: Elongate and Munch raise millions for various causes

The rise of crypto charities: Elongate and Munch raise millions for various causes- MoviePass Majority Owner Rises After Canaccord Says Buy

- 7 China-Based Stocks For High Growth At A Reasonable Price

WTI Crude Crumbles To Test $44 Handle As Algos Run Stops, Read DOE Report

WTI Crude Crumbles To Test $44 Handle As Algos Run Stops, Read DOE Report

Leave A Comment