Photo Credit: Mike Mozart

Wells Fargo & Company (WFC) Financials – Commercial Banks | Reports July 15, Before Market Opens

Big banks are in the spotlight this week with JPMorgan Chase, Wells Fargo and Citigroup all set to report quarterly earnings in the next 5 days. Wells Fargo, along with Citi, cap off the week with second quarter results Friday, before the market opens. Wells Fargo has been one of the more stable banks in recent years, maintaining relatively flat earnings and mid single digit revenue growth. Expectations are relatively muted this quarter as rates remain low and currency headwinds persist.

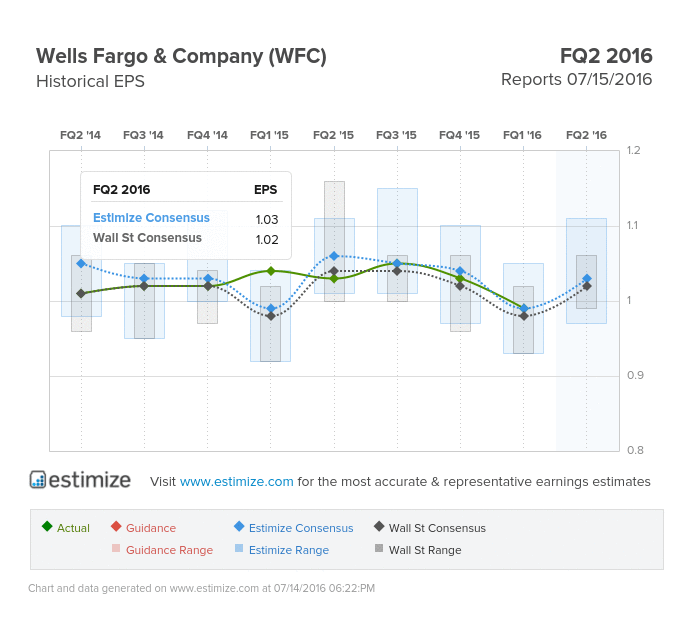

The Estimize consensus is looking for earnings per share of $1.03 on $22.27 billion in revenue, 1 cent higher than Wall Street on the bottom line and $40 million on the top. Compared to a year earlier this reflects a 7% decline in earnings and 3% in sales. Shares of Wells Fargo are down 5% year to date and typically fall 1% through earnings.

This year has been rough for the financial sector. Banks began 2016 expecting multiple rounds of interest rate hikes and a nice boost to net interest income. However a delay in Fed hikes coupled with Brexit uncertainty and falling oil prices in the early part of 2016 put earnings under extreme pressure. The stronger dollar resulting from certain macroeconomic events has also hampered profits.

Wells fargo’s earnings have been relatively resilient given it has little exposure to risky trading and investment banking businesses. Furthermore, the bank’s operations and investments are largely isolated compared to its large cap peers. Still the current economic landscape has caused the bank to reduce its profitability targets for the remainder of the year. Wells Fargo recently lowered its full year target return on assets to the range of 1.1% to 1.4%. The bank sees continued stress in its oil and gas portfolio this year with the potential for additional reserve increases or more credit losses.

Related Posts

The Chilly Reception Of Keurig Kold Has Analysts Reducing Their GMCR Estimates Into Tonight’s Report

The Chilly Reception Of Keurig Kold Has Analysts Reducing Their GMCR Estimates Into Tonight’s Report Experts say new South Korean crypto rules will create a monopolized market

Experts say new South Korean crypto rules will create a monopolized market 15 influential women entrepreneurs in Web3

15 influential women entrepreneurs in Web3 BT Group Price Swoons Overseas

BT Group Price Swoons Overseas EUR/USD Bullish Bounce At 1.15 Round Level Support

EUR/USD Bullish Bounce At 1.15 Round Level Support The U.S. Debt Problem Can No Longer Be Ignored

The U.S. Debt Problem Can No Longer Be Ignored

Leave A Comment