The House released an outline of a plan to make major changes to the current tax code last week – a move that is now making headline after headline as the plan heads through Congress and the president is prioritizing tax reform as a major part of his agenda.

So what is the plan as it now stands, and what might this mean for you? Take a look below to see some high-level changes being proposed.

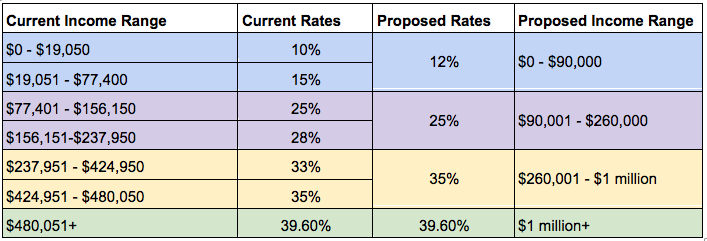

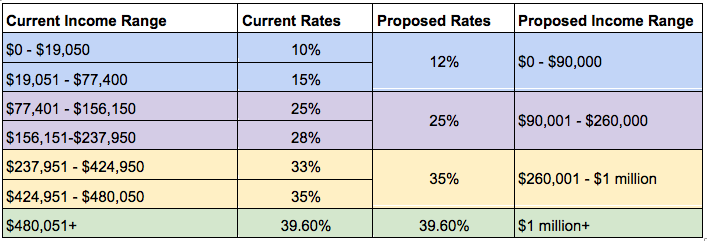

Married Couples Filing Jointly: 2017 vs. Proposed Tax Plan

Source: New York Times

Generally, the proposed plan lowers or maintains rates for five of the seven current income ranges, and increases rates in the other two. It also reduces the number of income tax brackets from seven to four.

Some other proposed changes include:

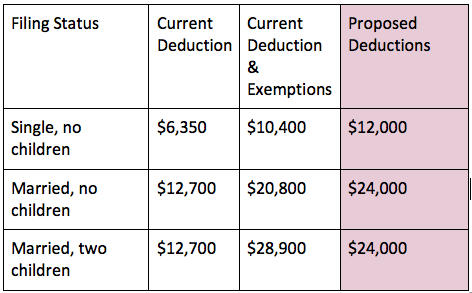

Standard Deductions – 2017 vs. Proposed Tax Plan

Source: New York Times; proposed deductions would increase with inflation in 2018.

If you are single, then the proposed plan will nearly double the standard deduction allowed, and eliminate the personal exemption (which is based on the number of taxpayers and the dependents claimed on a return).

Other changes proposed include:

Related Posts

E

J.C. Penney’s Go-Forward Strategy: Haven’t We Seen This Movie Before?

E

J.C. Penney’s Go-Forward Strategy: Haven’t We Seen This Movie Before?- McBride warns of second wave of material cost rises

Presenting 3 Chinese “Endgame Scenarios”

Presenting 3 Chinese “Endgame Scenarios” Stocks Set To Bounce Back, But Bulls’ Worries Far From Over

Stocks Set To Bounce Back, But Bulls’ Worries Far From Over- Daily Trading Opportunities – Friday, February 3

- Singapore saw 13x jump in crypto investments in 2021: KPMG

Leave A Comment