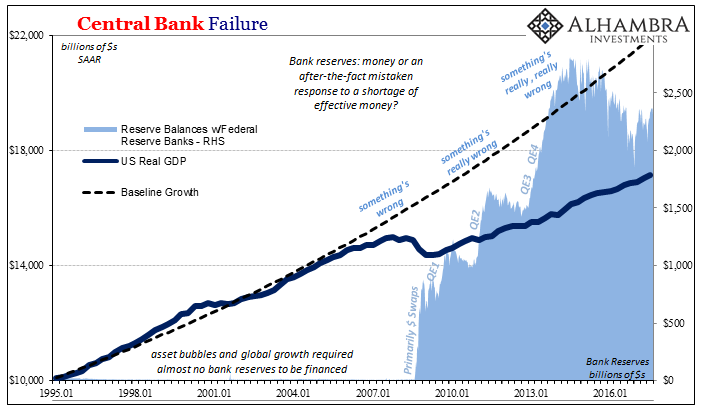

In mainstream monetary convention, bank reserves are at the center of the monetary pyramid. They are the byproduct of any central bank policy which requires direct action. In the US system, they had been absent, however, until around 2008. The reason was the Federal Reserve’s belief that it didn’t require any change in the corresponding balance of aggregate reserves to affect the main lever of pre-crisis monetary policy – the raising or lowering of the federal funds rate.

The market did it for them, which they mistook for uniform belief in central bank monetary supremacy; the theoretical threat of bank reserves, if you like. In other systems, the level of bank reserves was taken as a level or even measure of central bank-driven money supply.

What happened instead was something far different and stranger. The eurodollar system evolved its own set of reserves outside of the accepted concept.

That has had the effect of distorting a whole bunch of other facets of the global economic system. In China, for example, bank reserves still play the monetary role theorized for the US system. They are an important, vital even, piece of the monetary base.

But still, unlike the textbook version, China’s central bank does not have full control over them. Though they form the monetary basis for the vast Chinese banking system, the PBOC’s asset side of its balance sheet is literally foreign; as in foreign reserves.

On the surface, that seems more of an accounting detail than any concern for monetary policy. After all, these are assets owned and controlled by the PBOC. To claim that the forex basis for China’s monetary system is ultimately an exogenous factor directly contradicts established doctrine.

This is the primary issue of the eurodollar system, and the true privilege of it being dollar denominated. When we speak of what it means to have a dollar-based world, typically most commentary on the issue revolves around commodity prices, especially oil. The so-called petrodollar looms large simply because nobody seems to appreciate it as merely a subset of the wider issue.

Thus, China attempting to address the petrodollar with an alternate or even competing petroyuan is also misunderstood to a significant degree. Pricing commodities in a particular denomination isn’t nothing, but it’s attacking a symptom rather than the cause.

Trade gets done in dollars. To the extent that oil is priced in them, that is merely a reflection of the eurodollar’s supplanting of gold exchange after Bretton Woods. The primary problem with that former global monetary arrangement was that its designers (including John Maynard Keynes and Harry Dexter White) never formulated any way for global liquidity to expand, or contract, for given needs and requirements.

Related Posts

Most Active Equity Options And Strikes For Midday – Friday, February 23

Most Active Equity Options And Strikes For Midday – Friday, February 23 The Turkish Lira Rises After A Day Of Higher Interest Rates

The Turkish Lira Rises After A Day Of Higher Interest Rates 6 ETF Picks For September

6 ETF Picks For September The US Dollar Has Begun To Recoup After The Fall On Friday

The US Dollar Has Begun To Recoup After The Fall On Friday Short Setups If There Is A Short-Term Breakdown

Short Setups If There Is A Short-Term Breakdown A Fatal Accident Waiting To Happen: U.S. Healthcare

A Fatal Accident Waiting To Happen: U.S. Healthcare

Leave A Comment