Expedia Inc. (Nasdaq: EXPE) delivered a below average 6.4% ROE over the past year, compared to the 8.8% return generated by the Consumer Discretionary sector. Expedia’s results may indicate management is running an inefficient business relative to its peers, which may very well be the case, but it is important to understand what ROE is made up of and how it should be interpreted. Knowing these components may change your view on Expedia’s performance and future prospects. I show you exactly what I mean in my DuPont analysis below.

How To Calculate Expedia’s ROE

Return on equity measures a corporation’s profitability by revealing how much profit a company generates with the money shareholders have invested. Return on Equity or ROE is generally calculated using the following formula:

ROE = Net Income To Common / Average Total Common Equity

ROE is a helpful metric that illustrates how effective the company is at turning the cash put into the business into gains or returns for investors. However, it is important to note that ROE can be “manufactured” by management with the use of leverage or debt.

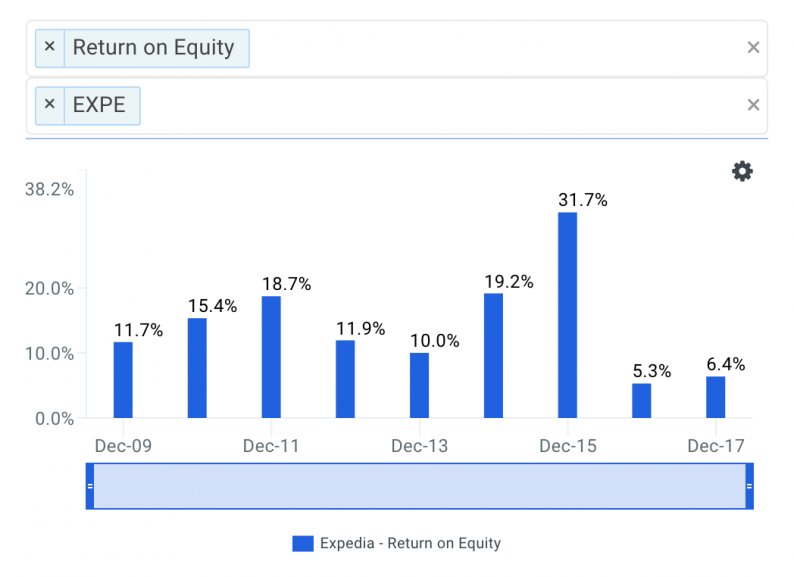

The return on equity achieved by Expedia over the last few years is shown below.

source: finbox.io data explorer – ROE

The finbox.io data explorer – ROE of Expedia has generally been declining over the last few years. ROE decreased from 31.7% to 5.3% in fiscal year 2016, increased to 6.4% in 2017 and the LTM period is also its latest fiscal year. So what’s causing the general decline?

Understanding Expedia’s Declining Return On Equity

The DuPont analysis is another way to calculate a company’s ROE using the following three metrics:

Return on Equity = Net Profit Margin * Asset Turnover * Equity Multiplier

Analyzing changes in these three items over time allows investors to figure out if operating efficiency, asset use efficiency or the use of leverage is what’s causing changes in ROE. Strong companies should have ROE that is increasing because its net profit margin and/or asset turnover is increasing. On the other hand, a company may not be as strong as investors would otherwise think if ROE is increasing from the use of leverage or debt.

Leave A Comment