At this point, I’m not really sure what counts as a “blowoff” top.

That term has been bandied about recently, and there are plenty of folks who will tell you they can define it, but that’s silly. It’s a Trump-ish superlative like “tremendous,” or “phenomenal,” or “big league.” Same goes for “melt-up.” What is a “melt-up,” exactly, if not what we’ve been seeing every single day for years? I don’t know. And contrary to what they’ll tell you, neither does anyone else.

“Later stages of bull markets are dominated by sentiment rather than valuations,” Bloomberg’s Tanvir Sandhu wrote earlier this morning. Duly noted, but please point me to a time over the last year when it would have been plausible to say that valuations at the index level were some semblance of compelling, because I must have been off the desk that day.

Anyway, the consensus seems to be that we’re entering some kind of “final phase” of the rally and it’s going to be a “tremendous,” “phenomenal”, “melting-up,” “bigly,” blow-off” top.

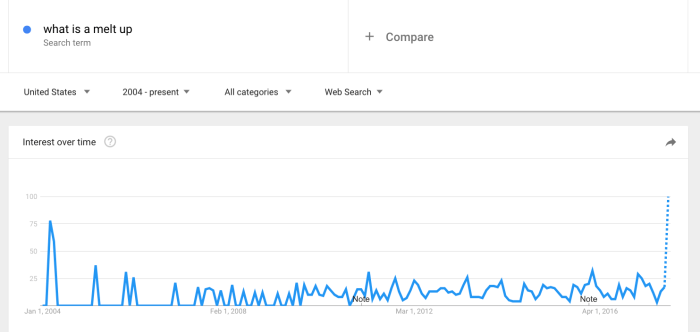

And do you want to see something super funny? Look at this Google Trends chart for the search term “what is a melt up?”

Yeah. “What is a melt up?” I’m willing to bet that exactly none of the people asking Google that question will come away with a satisfactorily definitive answer.

“Traders are positioning to chase equities into year-end for a possible rally that the popular press has termed as a ‘melt-up’ or ‘blowoff’ scenario [as] the equity market rally from the 2009 bottom has been the second longest, right after the one preceding the Dot-com crash, but the SPX keeps marching higher ignoring events that would have historically challenged the advance,” Deutsche Bank writes, in a new note, adding that “with valuations at record highs, and many risks still present ranging from geopolitical issues, failure on getting significant tax reforms done, re-emergence of debt ceiling discussions, etc., upside options provide a good way to retain long exposure while protected against downside risks.”

Leave A Comment