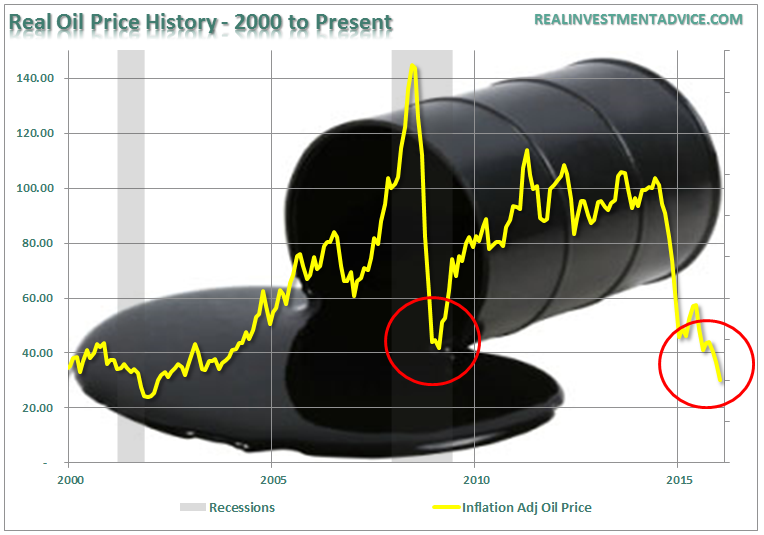

There is much hope in the financial markets, with individual investors and oil company employees that oil prices will rise in the months ahead. Many point to the 2008 commodity crash as THE example as to why the oil price decline is likely temporary.

However, if we look back further in history we see another situation where the crash in commodity prices marked an extremely long period of oil price suppression.

What was the difference? It was the supply to demand imbalance.

In 2008, when prices crashed, the supply of into the marketplace had hit an all time low while global demand was at an all-time high. The fears of “peak oil” were still a recent memory as the financial crisis took hold pushing prices to the lowest levels seen in years.

This supply-demand imbalance, combined with suppressed commodity prices, was the perfect cocktail for a surge in prices as the “fracking miracle” came into focus. The surge of supply alleviated the fears of oil company stability and investors rushed back into energy-related companies to “feast” on the buffet of accelerating profitability into the infinite future.

Banks also saw the advantages and were all too ready to lend out money for drilling of speculative wells. As investors gobbled up equity shares, the oil companies chased ever potential shale field in the U.S. in hopes to push stock prices higher. It worked…for a while.

The problem is now the supply-demand imbalance has reverted. With supply now back at levels not seen since the 1970’s, and demand waning due to a debt-cycle driven global economic deflationary cycle, the dynamics for a sharp rise in prices in the months to come is unlikely.

However, this is just assuming that current supply remains status quo. The problem, as I have discussed in the past, is that while the U.S. is curtailing CapEx and some production, it is being offset by production from China, Russia, and now Iran. According to the NYT:

Related Posts

U.S. Interest Rates

U.S. Interest Rates Silver Trading Strategy – XAGUSD Analysis & Forecast

Silver Trading Strategy – XAGUSD Analysis & Forecast Fed Balance Sheet Shrink: Big Problem Or Non-Event?

Fed Balance Sheet Shrink: Big Problem Or Non-Event? 4 Food Stocks Poised To Outshine The Market In 2018

4 Food Stocks Poised To Outshine The Market In 2018- Oil’s Rise And Its Impact On Other Sectors

Citi calls out potential risks of crypto-backed mortgages and benefits of metaverse property

Citi calls out potential risks of crypto-backed mortgages and benefits of metaverse property

Leave A Comment