I could see this coming a mile away…

Snapchat is already catching flak.

Its parent company, SNAP, IPO’d less than a week ago.

Founded in 2011, Snapchat is the photo-disappearing social media company with 158 million users who are typically between the ages of 18 and 24.

Its IPO was the biggest tech IPO since Alibaba’s (BABA) in 2014 and the biggest American tech IPO since Facebook’s (FB) in 2012.

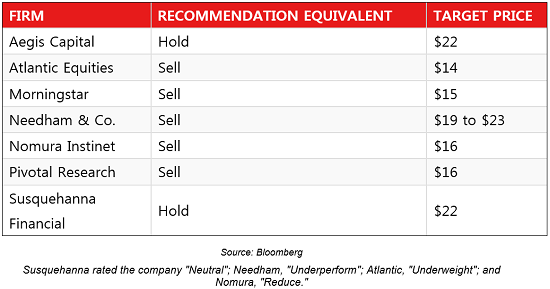

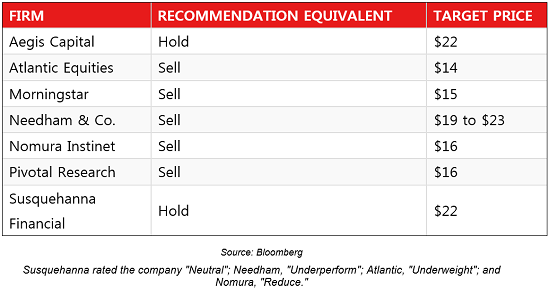

Not one broker among the eight following the company has a buy. Most have sells…

Snap’s Disappointing Ratings

Based on ratings as of March 6, five out of seven firms say Snap is a “Sell.”

The first day, its shares rose by more than 51% at their peak. The second day, they went up again. Since then, it’s been more down than up.

Boy, am I NOT surprised.

Apart from the pessimistic ratings, here are some reasons why…

I could go on, but I’ll stop right here.

BECAUSE ALL OF THIS IS MISSING THE POINT.

The Makings of a Future Social Media Powerhouse

Investors aren’t (or shouldn’t be) betting on Snap’s past or current performance.

They’re investing with a long-term view of Snap’s potential to develop into a future social media titan.

And nothing that has happened in the past week has made that future one iota less likely. Snap is absolutely dripping with upside.

It’s by far the best equipped social media company to reach out to the millennial generation.

This also happens to be the demographic that is watching less TV. Snap plans to recreate TV ads on mobile and grab a large chunk of the huge and growing TV ad budget.

In the U.S. alone, TV ads total more than $70 billion, says eMarketer. Worldwide, it was $652 billion in 2016. Snap states (in its S-1) that mobile advertising is its fastest-growing segment. It’s expected to grow 3X from $66 billion in 2016 to $196 billion in 2020.

Related Posts

Anti-Austerity Socialists Topple Portugal’s Two-Week Old Government; Modern Day Brezhnev Doctrine Review

Anti-Austerity Socialists Topple Portugal’s Two-Week Old Government; Modern Day Brezhnev Doctrine Review- Global Markets Turn Cautious, IPO News & Cues To Watch Out Today

Stocks And Precious Metals Charts – Repentance And Forgiveness The Wellspring Of Joy

Stocks And Precious Metals Charts – Repentance And Forgiveness The Wellspring Of Joy 18 Reasons To Buy Gold In 2018

18 Reasons To Buy Gold In 2018 WTI Crude Oil And Natural Gas Forecast – Friday, November 10

WTI Crude Oil And Natural Gas Forecast – Friday, November 10 EURUSD Posts Fresh Highs As Investors Feel Confident In The Euro

EURUSD Posts Fresh Highs As Investors Feel Confident In The Euro

Leave A Comment