WTI/RBOB held gains overnight following API’s reported crude draw (despite the gasoline glut) but after DOE confirmed a 5th weekly crude draw and 6th weekly gasoline build, algos were confused with prices chaotic. Production hit a new record high.

North Sea and Canadian crude supply disruptions are suppressing U.S. imports and encouraging exports.

API

DOE

This is the 5th weekly draw in crude in a row (and sixth weekly build in gasoline), perhaps the unexpected build in Distillates is spooking markets…

Bloomberg Intelligence energy analyst Fernando Valle:

Heightened U.S. refinery utilization is shifting the supply glut from crude inventories to refined products, particularly gasoline. Exports have risen, but are not enough to offset higher production and a seasonal demand slowdown.

Distillate demand, on the other hand, is rising, domestically and abroad. Crack spreads have stayed near $20 a barrel since Hurricane Harvey, which may lead refiners to shift gasoline yield toward distillates.

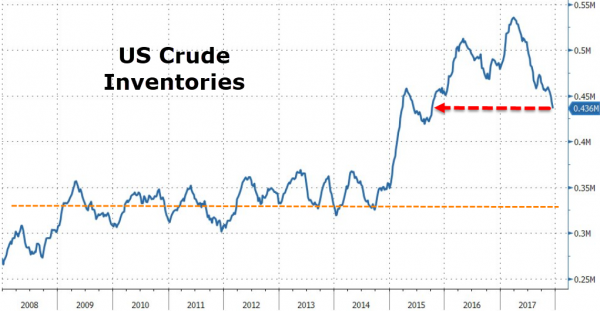

Total crude inventories are the lowest since Oct 2015 (but as is clear remain well elevated from old norms)…

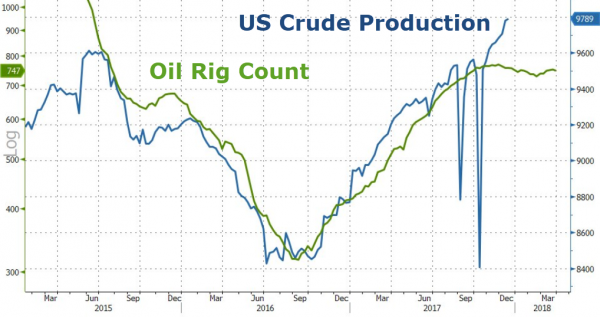

Production rose once again to a new record high…notably decoupled from rig counts now

WTI/RBOB prices remained higher post-API heading into the DOE data but the machines decide it was time to sell as the DOE data confirmed API (perhaps it is yet more crude production and the smaller than expected gasoline build)…

“The constructive surprise that may occur today would be a similar draw to the APIs in the EIAs for distillate,” Thomas Finlon, director of Energy Analytics Group, says. “There is some dreadful weather coming in the 5-15 day window.”

Leave A Comment