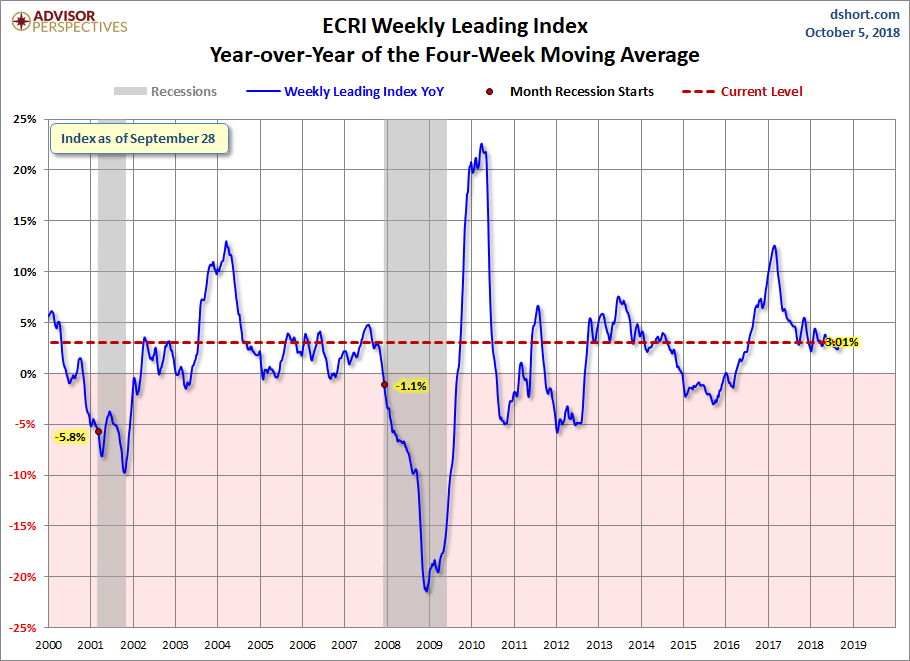

This morning’s release of the publicly available data from ECRI puts its Weekly Leading Index (WLI) at 149.1, up from the previous week’s 148.4. Year-over-year the four-week moving average of the indicator is now at 3.01%, down from last week. The WLI Growth indicator is now at 0.48, up from the previous week.

“Outsized Gains for Least Educated Limits Wage Growth”

ECRI’s latest article discusses the 10% of employed who do not have high-school diplomas, yet who have seen the most gains in employment since the recovery. From the article: “…In essence, the jobs recovery has been spearheaded by cheap labor”. Read more

The ECRI Indicator Year-over-Year

Below is a chart of ECRI’s smoothed year-over-year percent change since 2000 of their weekly leading index. The latest level is above where it was at the start of the last recession.

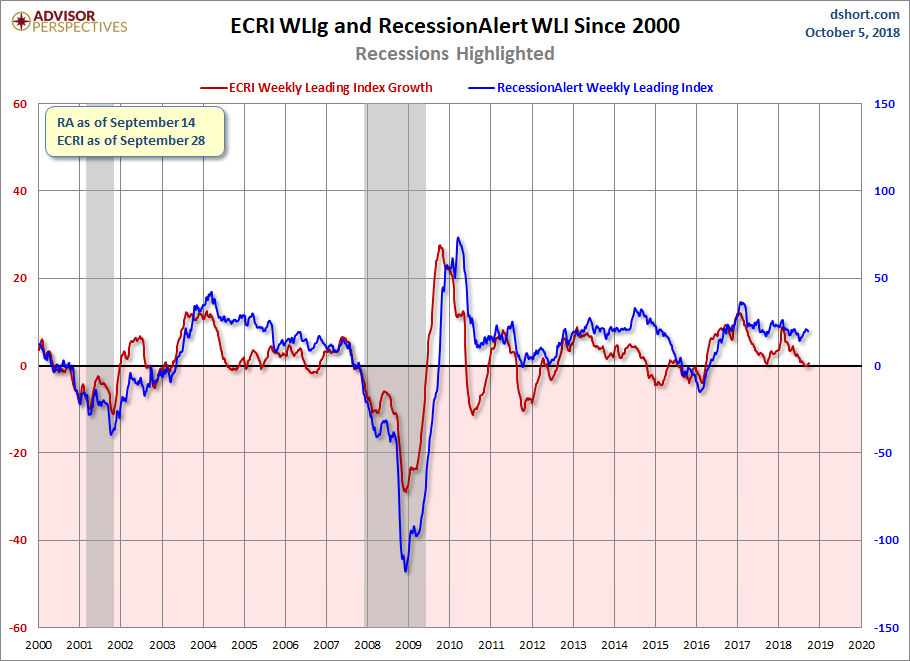

RecessionAlert has launched an alternative to ECRI’s WLIg, the Weekly Leading Economic Indicator (WLEI), which uses 50 different time series from various categories, including the Corporate Bond Composite, Treasury Bond Composite, Stock Market Composite, Labor Market Composite, and Credit Market Composite. An interesting point to notice — back in 2011, ECRI made an erroneous recession call, while the WLEI did not trigger such a premature call. However, both indicators are now generally in agreement and moving in the same direction. Frequently the latest RecessionAlert data is not available at publish time and will be posted at a later point.

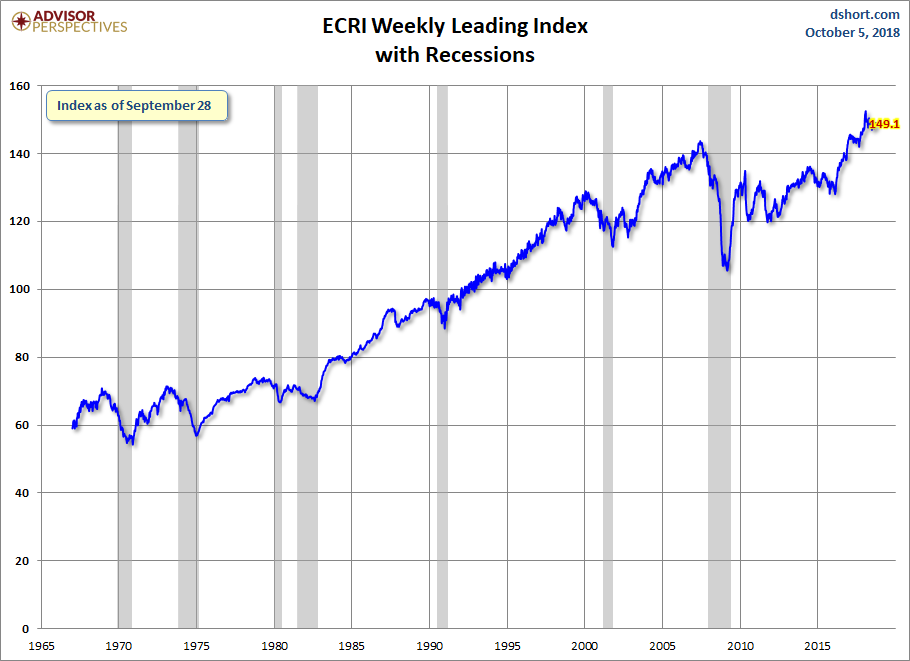

Appendix: A Closer Look at the ECRI Index

The first chart below shows the history of the Weekly Leading Index and highlights its current level.

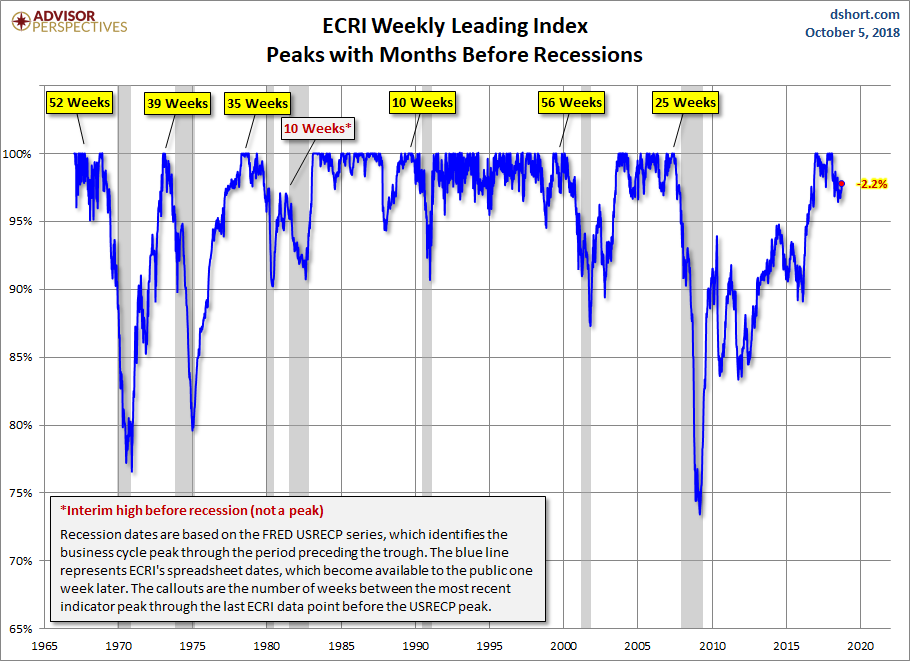

For a better understanding of the relationship of the WLI level to recessions, the next chart shows the data series in terms of the percent-off the previous peak. In other words, new weekly highs register at 100%, with subsequent declines plotted accordingly.

As the chart above illustrates, only once has a recession ended without the index level achieving a new high — the two recessions, commonly referred to as a “double-dip,” in the early 1980s. We’ve exceeded the previously longest stretch between highs, which was from February 1973 to April 1978. But the index level rose steadily from the trough at the end of the 1973-1975 recession to reach its new high in 1978. The pattern in ECRI’s indictor is quite different, and this has no doubt been a key factor in their business cycle analysis.

Related Posts

GasLog Transports Liquefied Natural Gas

GasLog Transports Liquefied Natural Gas The Best Trump Trade Wasn’t Made In America

The Best Trump Trade Wasn’t Made In America ECRI Weekly Leading Index: “Finding The Root Cause Of Recessions”

ECRI Weekly Leading Index: “Finding The Root Cause Of Recessions” Joe Sixpack’s Situation In 4Q2015: Joe Continues To Be Better Off

Joe Sixpack’s Situation In 4Q2015: Joe Continues To Be Better Off Bitcoin ETF hopium fades as on-chain and futures data reflect traders’ muted activity

Bitcoin ETF hopium fades as on-chain and futures data reflect traders’ muted activity Gold Slips As Stocks Swing

Gold Slips As Stocks Swing

Leave A Comment