Fundamental Forecast for EUR/USD: Neutral

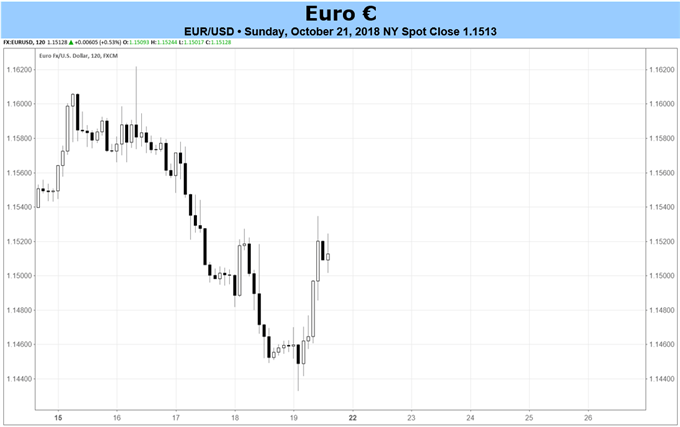

The Euro finished in the middle of the pack again last week, trading within +/- 0.5% against six of the other seven major currencies. The lone standout was EUR/NZD, which dropped by -1.74% as the aggregate impact of stronger New Zealand inflation figures and failure by the US Treasury to name China an FX manipulator gave ground for recovery in the antipodean currency (the second worst EUR-cross on the week was EUR/AUD, down by -0.47%). Two of the more popular pairs, EUR/GBP and EUR/USD, made little net progress, with the former adding +0.19% and the latter dropping by -0.40%.

As has been the case for most of October, the Euro remains a passenger on the recent rollercoaster of volatility. Like the week preceding it, the economic calendar yielded little insightful information, and while there were several news items related to the Italian budget, nothing concrete emerged; we’re essentially in the same place in the Italian budget saga as we were at the end of September. While investors continue to push up Italian BTP yields, the Euro has weathered most of the erosion in credit conditions, suggesting that a resolution to the budget saga would be a potent bullish catalyst.

While we expect Italy to remain a focal point in the days ahead, the coming week will be different than the week that preceded it, insofar as the economic calendar has meaningful information that typically moves FX markets as well as the October European Central Bank rate decision. With respect to the policy meeting, traders may want to temper expectations for significant price action developing. After all, there is no new set of Staff Economic Projections (those were received last month), which already biases the ECB towards inaction.

Related Posts

Talk Of A Crash

Talk Of A Crash AUD/USD Weekly Analysis – Tuesday, Oct. 30

AUD/USD Weekly Analysis – Tuesday, Oct. 30- GBP/JPY Advances To Near 184.40 On Downbeat Japanese Labor Cash Earnings Data

Cryptocurrency Driving Silver Demand

Cryptocurrency Driving Silver Demand Crypto Wrap: XRP Dips Amid SEC’s Appeal But Flare, Aptos See Gains

BTC struggles amid geopolitical crisis

SEC to appeal Ripple verdict; XRP dumps 14%

Crypto Wrap: XRP Dips Amid SEC’s Appeal But Flare, Aptos See Gains

BTC struggles amid geopolitical crisis

SEC to appeal Ripple verdict; XRP dumps 14%- The Latest Revolving Door Farce: Bernanke, Trichet And Gordon Brown To Form Pimco Advisory Board

Leave A Comment