Here is the latest update of a popular market valuation method using the most recent Standard & Poor’s “as reported” earnings and earnings estimates and the index monthly average of daily closes for the past month. For the earnings, see the table below created from Standard & Poor’s latest earnings spreadsheet.

The Valuation Thesis

A standard way to investigate market valuation is to study the historic Price-to-Earnings (P/E) ratio using reported earnings for the trailing twelve months (TTM). Proponents of this approach ignore forward estimates because they are often based on wishful thinking, erroneous assumptions, and analyst bias.

TTM P/E Ratio

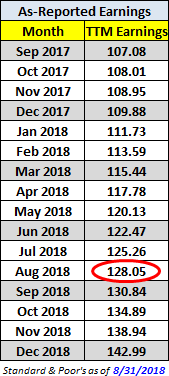

The “price” part of the P/E calculation is available in real time on TV and the Internet. The “earnings” part, however, is more difficult to find. The authoritative source is the Standard & Poor’s website, where the latest numbers are posted on the earnings page.

The table here shows the TTM earnings based on “as reported” earnings and a combination of “as reported” earnings and Standard & Poor’s estimates for “as reported” earnings for the next few quarters. The values for the months between are linear interpolations from the quarterly numbers.

The average P/E ratio since the 1870’s has been about 16.8. But the disconnect between price and TTM earnings during much of 2009 was so extreme that the P/E ratio was in triple digits — as high as the 120s — in the Spring of 2009. In 1999, a few months before the top of the Tech Bubble, the conventional P/E ratio hit 34. It peaked close to 47 two years after the market topped out.

As these examples illustrate, in times of critical importance, the conventional P/E ratio often lags the index to the point of being useless as a value indicator. “Why the lag?” you may wonder. “How can the P/E be at a record high after the price has fallen so far?” The explanation is simple. Earnings fell faster than price. In fact, the negative earnings of 2008 Q4 (-$23.25) is something that had never happened before in the history of the S&P 500.

Leave A Comment