Investors tend to not complain about a price rally, except when the chart presents steep downside risks. For example, analyzing Ether’s (ETH) current price chart could lead one to conclude that the ascending channel since March 15 is too aggressive.

For starters, the Ethereum network’s total value locked (TVL) peaked at ETH 32.8 million on Jan. 23, and has since gone down by 20%. TVL measures the number of coins deposited on smart contracts, including decentralized finance (DeFi), gaming, NFT marketplaces, social networks, collectibles and high risk.

Moreover, the Ethereum network’s average transaction fee bottomed at $8 on March 16, but has recently increased to $15. Thus, one must evaluate if that reflects lesser use of decentralized applications (DApps) or users benefiting from layer-2 scaling solutions.

Ether’s futures premium shows little excitement

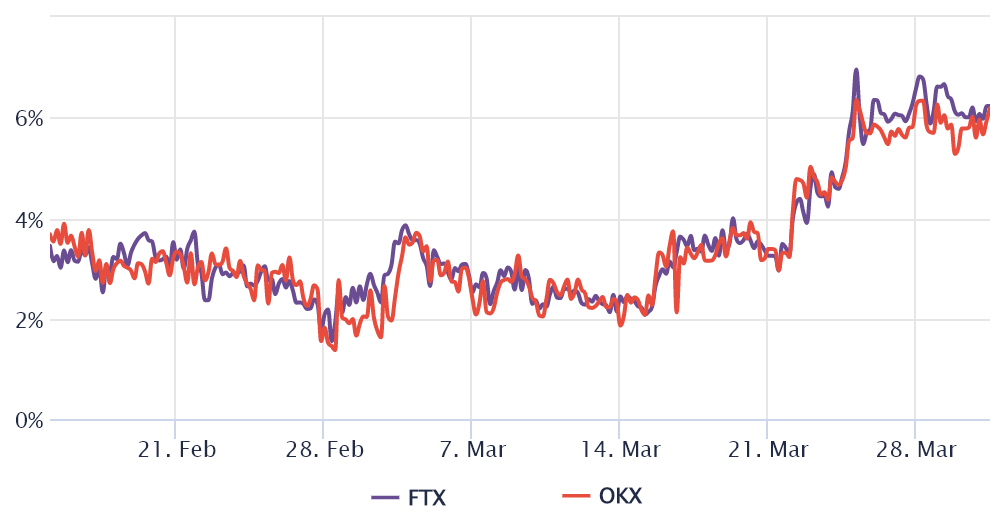

Traders should analyze Ether futures market data to understand how professional traders are positioned. The quarterly contracts are whales and market makers’ preferred instruments because they avoid the fluctuating funding rate from the perpetual futures.

The basis indicator measures the difference between longer-term futures contracts and the current spot market levels. The Ether futures annualized premium should run between 5% to 12% to compensate traders for “locking in” the money for two to three months until the contract expiry.

This data tells us that pro traders are far from excited but in the past couple of months there was a 4% or lower basis rate, which reflected bearish sentiment. Thus, there has been an improvement, but not enough to cause excessive demand from buyers.

To exclude externalities that might have influenced derivatives data, one should analyze the Ethereum network’s on-chain data. For example, monitoring the network use tells us whether actual use cases support the demand for Ether.

On-chain metrics raise concerns

Measuring the number of active addresses on the network provides a quick and reliable indicator of effective use. Of course, this metric could be misguided by the increasing adoption of layer-2 solutions, but it works as a starting point.

Traders should proceed to DApp usage metrics but avoid exclusive focus on the TVL because that metric is heavily concentrated on lending platforms and decentralized exchanges (DEX), so gauging the number of active addresses provides a broader view.

As a comparison, the DApps on the Polygon network gained 12% while Solana (SOL) saw a 6% user increase. Unless there is decent growth in Ether transactions and DApp usage, the $3,340 daily close support will probably unwind.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph. Every investment and trading move involves risk. You should conduct your own research when making a decision.

Leave A Comment